Amid turmoil in the financial sector and uncertainty ahead, the Federal Reserve will likely approve a 0.25 percentage point increase at this week’s policy meeting.

That will mark one year since the central bank began the current rate-raising cycle.

For consumers, that means they must still pay a higher price to borrow while continuing to grapple with a persistently high cost of living — all while suffering a crisis of confidence when it comes to their savings accounts.

“They are right in feeling these are dire economic times,” said Tomas Philipson, a professor of public policy studies at the University of Chicago and a former acting chair of the White House Council of Economic Advisers.

Incomes have not kept pace with inflation, which means purchasing power has declined as inflation has squeezed household budgets.

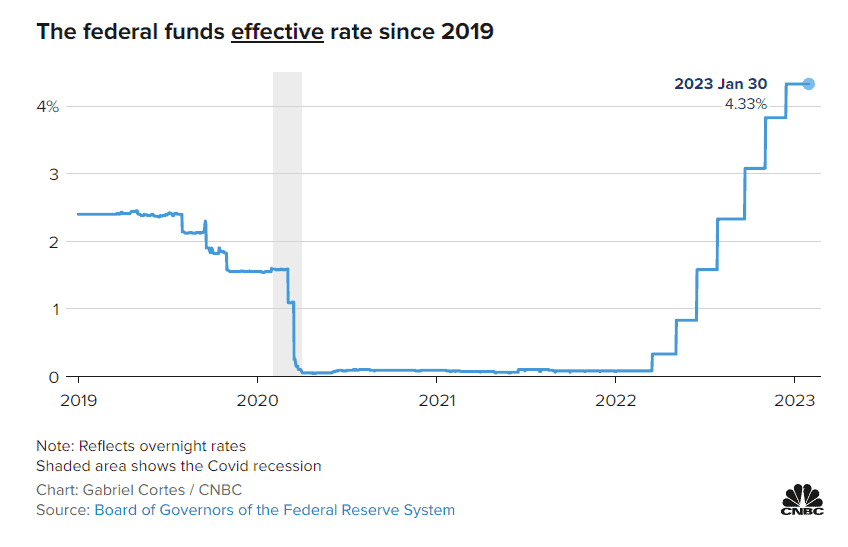

Rate hikes, one year later

For its part, the Fed has already hiked its benchmark fund rate eight times over the last year to its current level of between 4.5% and 4.75%.

The federal funds rate, which is set by the central bank, is the interest rate at which banks borrow and lend to one another overnight. But Fed rates also influence consumers’ borrowing costs, either directly or indirectly, including their credit card, mortgage and auto loan rates.

Average credit card rates now top 20%

Average credit card rates now top 20%

Since most credit cards have a variable interest rate, there’s a direct connection to the Fed’s benchmark. As the federal funds rate rises, the prime rate does, too, and credit card rates follow suit.

After a prolonged period of rate hikes, the average credit card rate is now over 20%, on average — an all-time high — up from 16.34% one year ago.

At the same time, households are increasingly leaning on credit to afford basic necessities, which makes it even harder for the growing number of borrowers who carry a balance from month to month.

Mortgage rates now average 6.66%

Although 15-year and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed’s policy moves.

The average rate for a 30-year, fixed-rate mortgage currently sits at 6.66%, up from 4.40% when the Fed started raising rates last March.

Auto loan rates rose to around 6.48%

Even though auto loans are fixed, payments are getting bigger because the price for all cars is rising along with the interest rates on new loans.

The average interest rate on a five-year new car loan is now 6.48%, up from 4% one year ago.

Federal student loans are already at 4.99%

Federal student loan rates are also fixed, so most borrowers aren’t immediately affected by rate hikes. The interest rate on federal student loans taken out for the 2022-23 academic year already rose to 4.99%, up from 3.73% last year, but any loans disbursed after July 1 will likely be even higher.

For now, anyone with existing federal education debt will benefit from rates at 0% until the payment pause ends, which the Education Department expects to happen sometime this year.

Private student loans tend to have a variable rate tied to the Libor, prime or Treasury bill rates — and that means that, as the Fed raises rates, those borrowers will also pay more in interest. How much more, however, will vary with the benchmark.

Deposit rates at banks can reach 5.02%

Thanks, in part, to lower overhead expenses, top-yielding online savings account rates are as high as 5.02%, much higher than last year’s 0.75%, according to Bankrate.

Although most savers don’t need to worry about the security of their cash at the bank, since no depositor has lost FDIC-insured funds due to a bank failure, any money earning less than the rate of inflation still loses purchasing power over time.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

{kind=link}