For more than twenty years, a quiet but incredibly expensive war has raged behind every cash register and digital checkout terminal in America. On one side stand the nation’s retailers, restaurants, and small business owners, who watch a slice of every sale vanish into thin air. On the other side sit global card giants Visa and Mastercard, backed by the powerful banking institutions that issue their plastic.

The first half of 2026 was supposed to be the moment the tide turned for merchants. Armed with new state legislation, a massive federal antitrust settlement, and bipartisan momentum in Congress, fee reformers believed they finally had the leverage needed to chip away at the card networks’ market dominance. Instead, the multi-billion-dollar payment industry successfully locked arms, fending off every major challenge. By mid-2026, the structural control exercised by Visa and Mastercard emerged entirely intact, leaving merchants to reckon with a harsh reality: the swipe fee fortress is harder to breach than ever.

Understanding the Financial Loop

To understand why this battle matters so much to your local economy, it helps to examine how money actually flows when you buy something. Every time a consumer runs a card through a terminal, the merchant does not receive the full purchase amount. Instead, they are hit with interchange fees (the processing charges, commonly known as swipe fees, that retailers pay to banks to handle card transactions).

As the transaction routes through the payment infrastructure, the money takes a round-trip journey. The card network coordinates the security and data protocols, while the card-issuing bank collects the bulk of the fee. Because Visa and Mastercard set these fee rates collectively for the banks that issue their cards, merchants argue that normal market competition is non-existent. Over a year, these micro-percentages pile up into tens of billions of dollars in overhead costs for businesses, which are frequently passed along to consumers through higher retail prices.

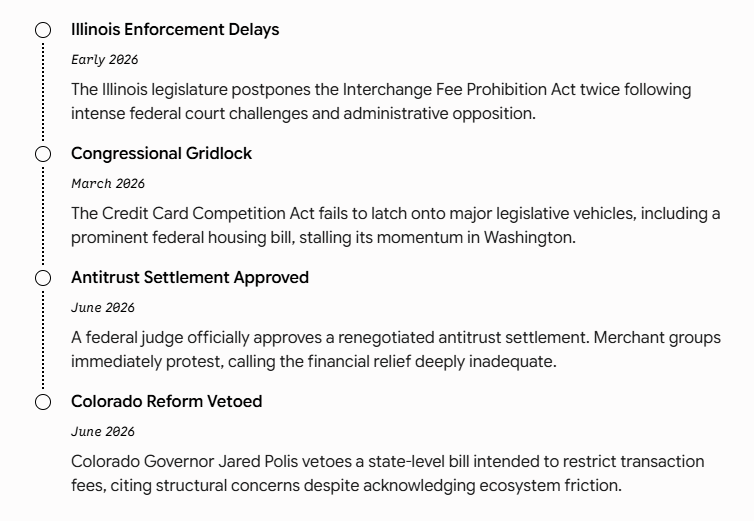

The State-Level Cracks in the Reform Movement

Frustrated by federal gridlock, merchant trade groups shifted their strategies toward state capitols over the last year. Lawmakers in both Colorado and Illinois attempted to take matters into their own hands, drafting ambitious state bills designed to directly curb the financial friction imposed by card networks. However, both initiatives hit major walls in the first half of 2026.

In Colorado, a highly anticipated bill aimed at reining in swipe fees passed the legislature, offering a glimmer of hope to local business coalitions. That hope vanished when Colorado Governor Jared Polis, a Democrat, officially vetoed the legislation. While Governor Polis expressed distinct sympathy for the merchants’ financial plight, noting in a lengthy veto letter that there is far too much friction in our transaction ecosystem, he ultimately determined that the specific state-level caps could create unintended operational issues inside the broader financial market.

Meanwhile, Illinois became a primary battleground for the Illinois Interchange Fee Prohibition Act. Supported heavily by Illinois Governor JB Pritzker, the law sought to exempt the tax and tip portions of transactions from swipe fees. However, implementation has been derailed by a wave of federal litigation (the process of resolving legal disputes through the court system). The state legislature has been forced to postpone the law twice this year. Compounding the state’s legal headaches, the measure ran into direct opposition from the Trump administration, stalling what was once considered the country’s most aggressive state-level fee reform.

A Federal Settlement Sparking Merchant Outrage

While state laws sputtered, a monumental development unfolded in federal court. A long-running class-action antitrust lawsuit (a legal action targeting anti-competitive monopolies to restore fair market play) finally reached a major milestone. A federal judge formally approved a renegotiated pact between the card company defendants and merchant plaintiffs.

While a court-approved settlement sounds like a victory on paper, the reality on the ground feels very different for the businesses affected. Retailers across the country widely panned the deal, arguing that the renegotiated terms offer negligible financial relief and fail to alter the underlying rules that keep swipe fees artificially high. The dissatisfaction echoed clearly across the hospitality sector. Sean Kennedy, the chief advocacy officer for the National Restaurant Association, voiced the widespread frustration of small business owners shortly after the judge’s decision:

“This settlement does little to address the problem of the anti-trust lawsuit that got us here and doesn’t provide true relief to the small business restaurant owners who are struggling to manage swipe fees.”

Stagnation on Capitol Hill

Merchants also looked to Washington for a structural remedy via the Credit Card Competition Act (CCCA). Championed by an unusual bipartisan alliance featuring Democratic Senator Dick Durbin of Illinois and Republican Senator Roger Marshall of Kansas, the bill aimed to break the Visa-Mastercard duopoly by requiring large banks to offer at least two competing processing networks on credit cards.

Despite securing public support from President Donald Trump, the CCCA has completely stalled in Congress. Lawmakers tried aggressively to attach the payment reform package to a massive, must-pass federal housing bill earlier this year. However, the Senate ultimately stripped the credit card provisions out, passing the housing package without them.

The legislative stall highlights the massive lobbying muscle wielded by the financial sector. Card networks and banking associations successfully framed the CCCA as a threat to popular consumer credit card reward programs, shifting political momentum away from the merchants.

The 2026 Timeline of Swipe Fee Defeats

The legal and political setbacks hitting fee reformers in the first half of this year showcase the resilience of the card networks’ defense strategy.

What Lies Ahead for the Fee Fight

Even the federal regulatory apparatus has moved at a crawl. A separate proposal introduced by the Federal Reserve to reduce the caps on debit card transaction fees has faced unexplained delays, leaving retailers without regulatory relief heading into the summer shopping season.

Yet, merchant advocates insist the fight isn’t over. There is a strong possibility that the Illinois attorney general will file an appeal to challenge the federal court rulings that are stalling their state fee law. Furthermore, the clock is ticking for Senator Dick Durbin. The Illinois Democrat, who has spent decades leading the charge against swipe fees, is set to conclude his congressional career in January 2027. Observers expect Durbin to make one final, aggressive push to pass the Credit Card Competition Act before his term expires.

For now, Visa, Mastercard, and their issuing banks remain firmly in control of the transaction landscape, proving that changing the rules of modern commerce requires more than just local friction—it requires a total structural overhaul.

Sources Used

- Payments Dive: Visa, Mastercard fend off fee foes

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

")

")

")

{kind=link}