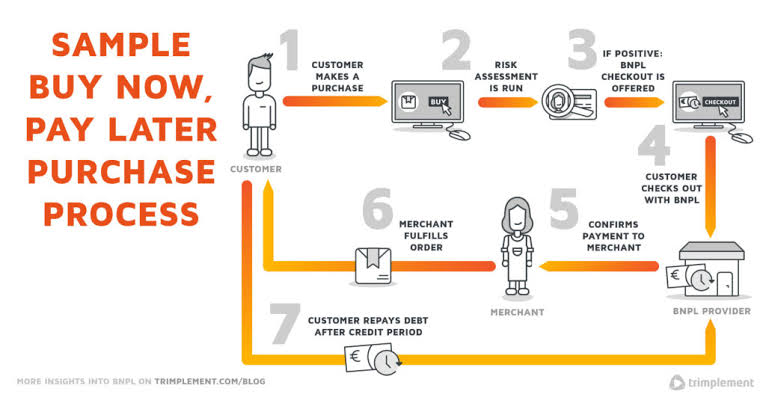

As illustrated in the transaction flow diagram below, the Buy Now, Pay Later (BNPL) system relies on a tightly integrated loop where a provider facilitates instant point-of-sale credit, paying the merchant immediately (minus a processing fee) and collecting scheduled installments from the consumer over time. While this seems like a win-win for both parties, a deeper economic look reveals a hidden structural side effect: this transaction loop is quietly driving up retail prices for all consumers.

The Reality of Merchant Fees

For millions of shoppers, BNPL platforms like Klarna, Affirm, and Afterpay have revolutionized online checkouts. Marketed as frictionless, interest-free alternatives to traditional credit cards, these services allow consumers to split a purchase into four biweekly installments. However, this “free” payment method hides a significant macroeconomic catch.

While shoppers pay no interest on timely payments, the service is far from free to operate. The bulk of BNPL revenue comes from steep merchant fees. Traditional credit card transactions typically cost merchants an interchange fee of 1.5% to 3%. In contrast, BNPL providers charge retailers a massive transaction fee ranging from 5% to 8%. To maintain profit margins under these heavy costs, merchants face a difficult dilemma. Because major merchant agreements heavily restrict or outright ban charging a surcharge specifically to BNPL users, retailers cannot easily pass these fees directly to the individuals utilizing the payment method.

The Cross-Subsidization Trap

Instead, businesses adapt by raising baseline retail prices across the board. This creates a highly regressive economic phenomenon known as cross-subsidization. Consumers who pay with lower-cost payment methods—such as cash, checks, or standard debit cards—end up paying inflated retail prices to cover the merchant transaction fees generated by BNPL users. This transfer mechanism mirrors the classic cross-subsidy found in credit card rewards programs, but at a much higher scale because of BNPL’s premium merchant rates.

Beyond fee pass-throughs, BNPL directly alters consumer behavior, feeding an upward price spiral. Behavioral finance research shows that splitting payments into bite-sized installments reduces a buyer’s psychological resistance to spending. This is known in economics as reducing price elasticity. When consumers focus only on a $25 installment instead of a $100 total price tag, they become far less sensitive to the overall cost.

Academic studies confirm that BNPL availability increases merchant sales by an average of 20%, driven heavily by consumers with lower creditworthiness. Because consumers are less sensitive to total prices when using installment plans, merchants gain increased pricing power. When demand remains highly inelastic despite higher price points, retailers are structurally incentivized to permanently raise prices on items frequently bought via BNPL, such as apparel, consumer electronics, and home goods.

Ultimately, the surge of BNPL is reshaping retail pricing models. What appears on the surface to be a consumer-friendly, interest-free budgeting tool acts under the hood as an inflationary force. As BNPL becomes increasingly integrated into both e-commerce and brick-and-mortar storefronts, cash and debit card users will continue to subsidize the premium processing costs of installment financing, resulting in higher price tags for everyone.

Sources and Links:

- National Bureau of Economic Research (NBER) Working Paper Series: Paper: “The Economics of ‘Buy Now, Pay Later’: A Merchant’s Perspective” (Tobias Berg, Valentin Burg, Jan Keil, and Manju Puri, 2024) Link: https://www.nber.org/system/files/working_papers/w33152/w33152.pdf

- Bank for International Settlements (BIS) Quarterly Review: Paper: “Buy now, pay later: a cross-country analysis” (Giulio Cornelli, 2023) Link: https://www.bis.org/publ/qtrpdf/r_qt2312e.htm

- Harvard Business School Working Paper: Paper: “Buy now, pay later credit: User characteristics and effects on spending patterns” (Marco Di Maggio, Emily Williams, and Justin Katz, 2022) Link: https://www.hbs.edu/ris/Publication%20Files/Buy%20now,%20pay%20later%20credit_EW_a84b3c98-3608-4f28-a534-8545246ac522.pdf

- Federal Reserve Bank of Kansas City Economic Review: Paper: “Financial Constraints Among Buy Now, Pay Later Users” (Fumiko Hayashi and Rachel Routh, 2024) Link: https://www.kansascityfed.org/documents/10891/EconomicReviewV110N4HayashiRouth.pdf

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

")

")

{kind=link}