Written by Carol J Alexander , Edited by Adam Graham , Reviewed by Irena Martincevic

For most Americans, a home purchase is the largest investment they’ll ever make. According to the U.S. Census Bureau, the median sales price of a new house was $430,700 in March 2024. When spending that much money, homeowners want to protect their investment, particularly with increased natural disasters like hurricanes, tornadoes, and wildfires. That protection comes in the form of homeowner’s insurance.

In this article, we examine how homeowner’s insurance protects against the cost of natural disasters and the cost of homeowner’s insurance in disaster-prone areas of the country. We also explore the worrying trend for homeowners in which major insurers are stopping renewing policies in extreme weather states. Then, we speak to experts to offer solutions for when coverage is denied.

State-Specific Insurance Challenges in 2024

Homeowners want to know what situations their policy covers, if they have enough coverage, and if the premiums are fair. But for those living in disaster-prone areas, waiting for a life event to examine a policy could work against them. “It’s important to ask questions before your annual renewal, or a nonrenewal, to ensure the best long-term placement,” says Christopher Giuditta, vice president and senior advisor at World Insurance.

While the cost of homeowner’s insurance depends primarily on the location, the size of the residence, and the amount of coverage, the national average cost to insure a home for $300,000 is $2,153 annually or $179 per month. However, the cost of adequate homeowner’s coverage increases significantly each year. For instance, from 2020 to 2021, premiums rose by 7.6% nationwide, according to a 2023 report by the National Association of Insurance Commissioners (NAIC).

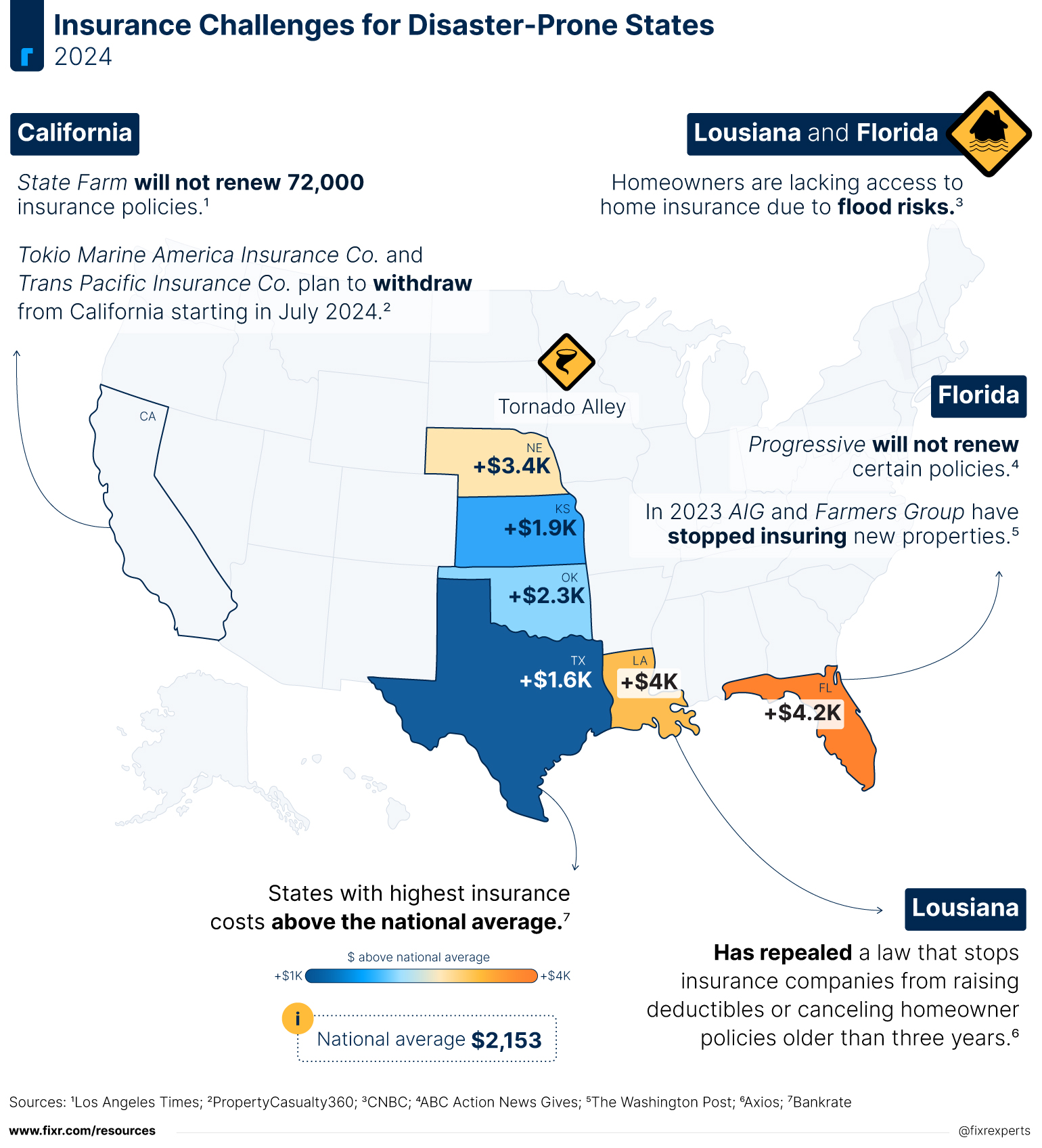

If someone lives in a disaster-prone area, they may need help with their homeowner’s coverage. In addition to Farmers, other major insurance carriers, like State Farm and Allstate, have ceased writing new policies in states prone to wildfires and floods because the cost to fulfill claims jeopardizes their ability to cover claims in other areas. Most of these problems occur in California, Florida, and Louisiana.

California

California experienced record-breaking wildfire seasons in 2017 and 2018, with over $12 billion in losses in 2018 alone. Since then, policy cancellations have steadily risen. The situation is so dire homeowners struggle to insure their homes due to rising costs and premiums costing tens of thousands of dollars.

Florida

Across the continent, the East Coast state of Florida has its own troubles. As a peninsula bordered by the Atlantic Ocean on the east and the Gulf of Mexico on the west, Florida is prone to extreme weather events, especially hurricanes. Consequently, the insurance industry in that state has lost 11 property and casualty companies since 2017. And in the past four years, over 30 companies have withdrawn their services or at least limited their lines of coverage.

In addition to its already tenuous position due to weather-related events, the state has seen an increase in other factors contributing to its insurance crisis. Insurance fraud tops the list. According to the Florida Office of Insurance Regulation’s 2023 Property Insurance Stability Report, in 2021, 7% of all homeowner’s insurance claims filed nationwide came from Florida. However, the majority of lawsuits over claims filed, 76%, also came from Florida.

According to Stacy Giulianti, chief legal officer at Florida Peninsula Insurance Company, the future is optimistic. “The governor and legislature have done a tremendous job to bring our legal and claims environment more in line with the rest of the nation, and we are already seeing lawsuits and spurious claims fall dramatically.” Giulianti is optimistic that Florida will see “rate stabilization and increased capacity in the very near future.”

Louisiana

Another state bordering the Gulf of Mexico, Louisiana, was hit by a series of hurricanes in 2020-2021. Ever since then, the insurance industry in that state has gone downhill. According to the Insurance Information Institute, “Twelve insurers that write homeowners coverage in Louisiana were declared insolvent between July 2021 and February 2023.” That doesn’t include the dozen insurers that have quit serving the state or the 50-plus to stop writing new business.

Elsewhere

The rest of the country’s future looks bleak. According to the National Oceanic and Atmospheric Administration (NOAA), 2023 holds the record for the most $1 billion disasters in a calendar year. Besides being the 5th warmest year on record, the U.S. experienced 28 separate weather and climate events, with damages costing $93 billion. Consequently, insurers are pulling out of, non-renewing, or limiting their offerings across the country.

Both Florida and Louisiana are the most expensive states with insurance costs exceeding $4K above the national average. Nebraska follows this with costs at $3K above the national average and Oklahoma has costs of over $2K higher. Both Kansas and Texas insurance costs exceed the average by over $1K. Vermont is the cheapest state with a cost of $1,347 below the national average.

According to Michael Orefice, senior vice president of operations at SmartFinancial, property insurers have stopped renewing policies in nine states: Arkansas, California, Colorado, Louisiana, Minnesota, Oklahoma, South Carolina, South Dakota, Florida, and Washington. Other sources add North Carolina, Arizona, and Nevada as problematic areas.

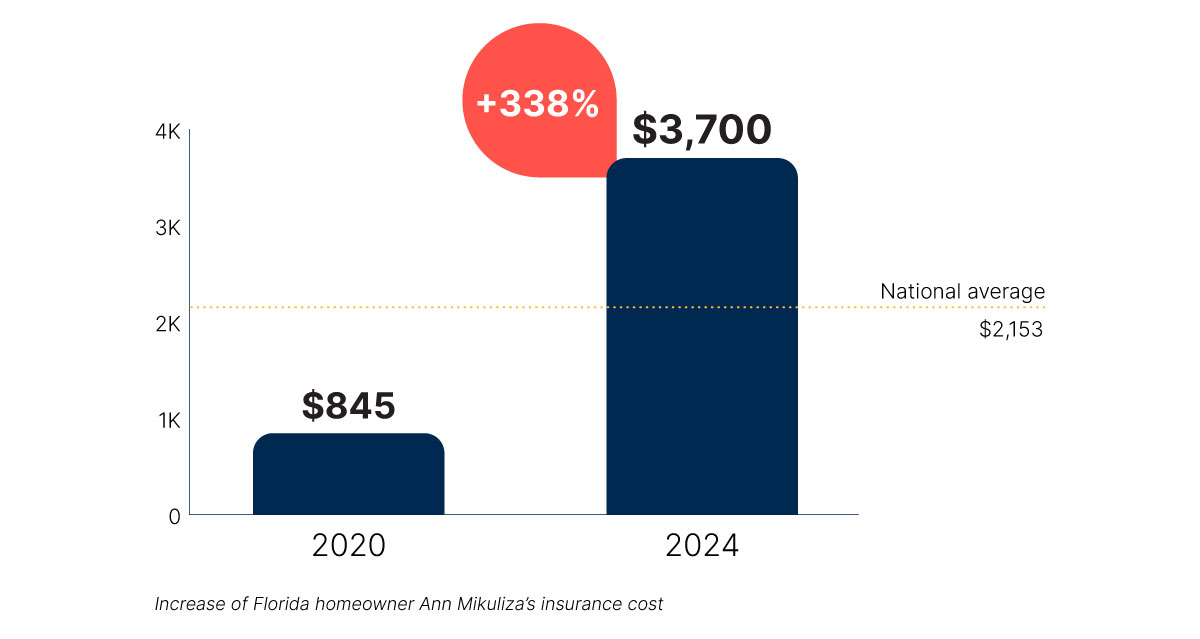

Real-Life Perspective: A Florida Homeowner

In 2020, Mikuliza paid $845 per year to insure her home with almost 100-year-old Farmer’s Insurance. She would’ve welcomed the nationwide 7.6% increase in 2021. Today, however, Farmer’s no longer writes policies in Florida, and Mikuliza is now paying $3,700 per year – an increase of 338%. And her new insurer is only three years old. Not exactly a name that’s earned public trust.

Unfortunately, Mikuliza’s experience is typical for homeowners in states that experience frequent natural disasters. Her advice? Shop around with different agents and do your research to find the best possible deal.

Homeowner’s Insurance: Natural Disaster Coverage

Homeowner’s insurance covers losses and damages to a home, its contents, and any other private structures, like a detached garage or garden shed. It also includes liability coverage against accidents incurred on the property. So, if a guest falls down the stairs or a shopper at a yard sale twists an ankle in a pothole, the homeowner is covered. However, in the U.S., only 93% of homeowners have some form of home insurance.

When a home suffers damage, homeowners expect their insurance to cover the cost. However, homeowner’s insurance typically only covers a particular set of circumstances. Coverage for other types of disasters costs extra. Here is a breakdown of what homeowner’s insurance normally does and does not cover.

What homeowner’s insurance typically covers

For the most part, you’ll find homeowner’s insurance covers damage incurred during the following catastrophic events.

- Wildfires

- Ice, snow, and deep freeze

- Lightning strikes

- Wind and hail

- Wind damage from hurricanes

- Volcanic eruptions

- Falling trees or branches

What homeowner’s insurance typically excludes

Notice that the above list doesn’t include some types of disasters. Standard property coverage typically excludes floods and earthquakes.

Some states require flood coverage if a home sits in a floodplain. A floodplain is a flat area of land adjacent to a river or stream, stretching from the river channel to the furthest reach of the valley. Separate coverage for both of these events is available through the National Flood Insurance Program (NFIP) or private insurers.

RELATED: Interactive Disaster Map: How to Prepare for Natural Disasters in Your State

Insurance Solutions for Denied Coverage

Homeowners who’ve lost coverage need solutions. But waiting for that to happen is not wise. “Don’t wait until it’s too late to play offense instead of defense,” says Giuditta. If someone lives in a disaster-prone area of the country, he suggests that “homeowners be proactive, take pride in ownership, and maintain their home for insurance carrier approval.”

If you don’t, insurance companies will demand it. When Mikuliza shopped for insurers to replace Farmer’s, she was asked about the age and condition of her roof, hot water heater, and air conditioning unit. “They would not insure me if my a/c was older than 10 years,” she said.

Fortunately for her, those items checked out fine. What didn’t was her piping.

Between 1978 and mid-1995, Polybutylene (PB) plastic was used for home plumbing systems due to its affordability, flexibility, and resistance to freezing. However, by mid-1996, contractors ceased using it due to pipe ruptures and ensuing property damage. Mikuliza’s home was built in 1993, and it has PB piping. Numerous insurance companies denied her coverage unless she replaced it. Her piping, as well as other items insurers questioned, has nothing to do with mitigating damage from natural disasters but everything to do with controlling other risks. The quotes she received to replace the pipes ranged from $5,000 to $10,000.

A homeowner struggling to find coverage should contact their state’s insurance department. It can provide a list of insurers that write policies in the area. “It might also have information regarding community groups that help homeowners with insurance problems, such as NeighborWorks America,” says Giuditta.

Here are a few options for those who struggle to insure their homes.

FAIR plans

Some states offer Fair Access to Insurance Requirements (FAIR) Plans to homeowners who’ve lost coverage. These plans are backed collectively by all the private insurers licensed to do business in the state, allowing multiple companies to share the risk of loss and any profits. To qualify, homeowners must demonstrate rejection by multiple carriers.

There are a few downsides to FAIR Plans. Typically, they include higher premiums for less coverage than voluntary market options. “A FAIR Plan policy protects a home from the risk of fire and will satisfy a mortgage company’s requirement that a home be insured, but it doesn’t cover theft, flood, earthquake, hail, vandalism or personal liability,” says Guiditta. However, additional coverage for contents and outbuildings may be offered as additional add-ons, depending on the state.

Also, homeowners frequently have to perform repairs or upgrades to the property in order to qualify for FAIR Plan coverage. Upgrades could include tasks like removing vegetation or replacing a roof. For some homeowners, like low-income, disabled, or the elderly, this could prove a hardship. And since FAIR Plan coverage is a last resort, they don’t have the option of finding someone else, as Mikuliza did. They have to make the repair or remain uninsured.

Surplus lines insurance

When regular insurers decline coverage for homes due to high risk, some states allow surplus lines insurance, a specialized coverage written by companies licensed in other areas but not the resident state. Surplus lines insurers include other U.S. insurers, companies affiliated with Lloyd’s of London, and non-U.S. insurers in the National Association of Insurance Commissioners (NAIC) Quarterly Listing of Alien Insurers. These providers must be licensed in their location, and the broker who sells the insurance must also be licensed.

If a homeowner faces several rejections from traditional insurers, usually three to five, they might qualify for surplus lines insurance. However, these policies often come with higher deductibles and more exclusions.

Where to Go From Here

According to a study by Stanford University’s Institute for Economic Policy Research (SIEPR), “California lost a net of 407,000 residents to other states between July 2021 and July 2022.” However, the whys and wherefores are more complicated than the insurance cost. If it were that simple, Florida, a state with a far more complex insurance landscape, wouldn’t continue to be the country’s top moving destination, with a net population gain of nearly 240,000 people in 2022.

One thing’s for sure: Homeowners need a sound understanding of the climate where they live or intend to live. Before purchasing a home in a disaster-prone area, they should secure quotes for homeowners insurance to accurately calculate the cost of ownership. Long-standing homeowners must also stay informed of current, local insurance industry news. When questions arise, consult with the state’s insurance department.

John Espenschied, owner of Insurance Brokers Group in Missouri, says, “There’s a need for collaborative efforts among governments, the insurance industry, homeowners, and communities to address these challenges.” The goal, he says, is “to ensure that every homeowner has access to the insurance coverage they need to protect their homes and families against the unexpected.”

Source: News Release

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

’ Has a New Idea to Get You Saving for Retirement")

{kind=link}