Predictions of a stabilizing rental market are coming closer to reality after rental data from September showed national rent prices trending down month-over-month for the first time this year.

In addition to price drops nationally, 61 percent of state-level markets saw decreased rents in September compared to August. New York saw the largest decrease at just over 17 percent month-over-month, with Illinois and Massachusetts experiencing the next biggest drops at 4.6 percent and 4.0 percent, respectively. Of the 50 metros analyzed in this report, 31 were down month-over-month. Cincinnati and Columbus, OH, led month-over declines with drops of nearly 7 and 6 percent, followed by the Los Angeles, CA, metro which decreased by 3.5 percent.

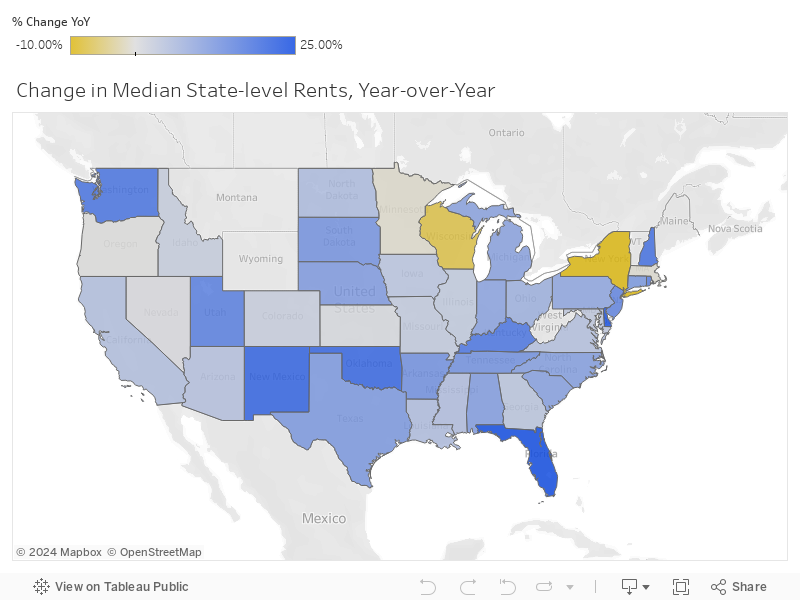

Year-over-year rents are still elevated, but prices are moderating. Nationally, rents are up 8.8 percent compared to last year, the first time in 2022 that yearly increases have touched the single digits. Minnesota and Wisconsin both saw lower median rent prices across their respective states driven by rent price decreases in the Minneapolis and Milwaukee metros. New York led state-level drops with a 10 percent rent decrease year-over-year.

Let’s look at where rent prices stand today.

National rent price trends

Nationwide, September rent prices are down month-over-month, a hopeful sign that the rental market is stabilizing.

Year-over-year increases slowed nationally, up 8.8 percent in September compared to a 12.3 percent increase in August. It’s the first time year-over-year changes dipped into the single digits since September 2021 and the lowest year-over-year increase since October 2021. Rents peaked during that time at a 17.5 percent increase in March 2022.

| Rental Market Summary | September 2022 | Month-over-Month | Year-over-Year |

|---|---|---|---|

| Median Monthly Rent | $2,002 | -2.5% | 8.8% |

State rent price trends

On a state level, median month-over-month is down in just over 60 percent of markets, a promising sign of a market beginning to cool. Year-over-year numbers are still up in nearly all but a few markets. Only New York, Wisconsin, Minnesota, Massachusetts and Oregon showed year-over-year declines, with only New York and Wisconsin down by more than a full percentage point at -10.01 percent and -7.39 percent respectively.

| Rental Market Summary | Markets Up | Markets Down |

|---|---|---|

| Year-over-Year (September 21 vs 22) | 88.64% | 11.36% |

| Month-over-Month (September vs August) | 38.64% | 61.36% |

Year-over-year state increases

With nearly 90 percent of markets up year-over-year, the largest increases are spread across the country. From Florida to New Jersey, Delaware to New Mexico and Washington to Rhode Island, rents are up by more than 15 percent. In total, 22 states saw year-over-year increases above the national median. Among those, 17 states saw a rent increase of more than 10 percent, and four states registered rent growth greater than 20 percent.

- Florida (+25.5 percent)

- Delaware (+23.9 percent)

- New Mexico (+21.2 percent)

- Oklahoma (+20.8 percent)

- New Hampshire (+19.1 percent)

- Washington (+18.4 percent)

- Kentucky (+18.3 percent)

- Utah (+16.7 percent)

- Rhode Island (+16.5 percent)

- New Jersey (+15.5 percent)

Year-over-year state decreases

Only five states saw rents decline in September year-over-year. Minnesota saw a 0.9 percent state-level decrease driven by a -8.8 percent decrease in the Minneapolis metro. Wisconsin rents dropped more than seven percent following a more than 14 percent drop in Milwaukee metro area rents. New York also saw state-level declines despite more than 15 percent growth in the New York City metro.

- New York (-10.0 percent)

- Wisconsin (-7.4 percent)

- Minnesota (-0.9 percent)

- Massachusetts (-0.6 percent)

- Oregon (-0.1 percent)

Metro areas rent price trends

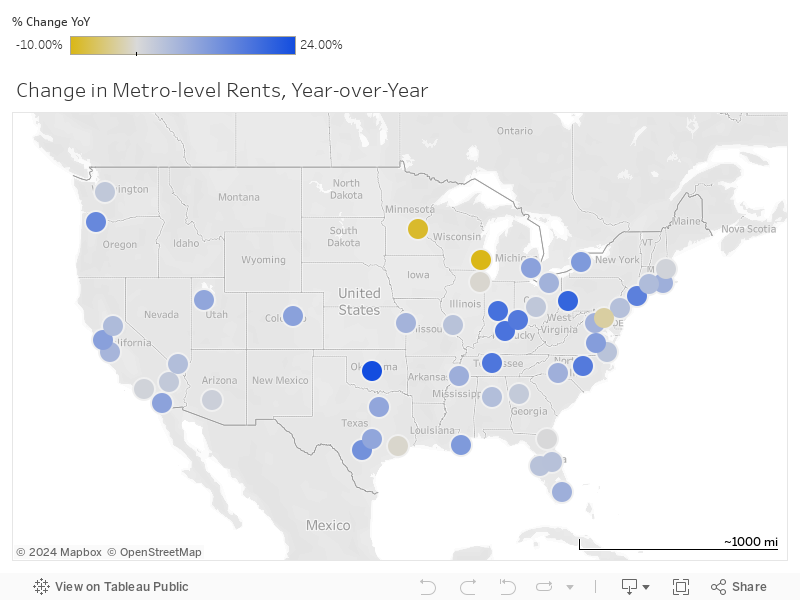

In the 50 most populous U.S. metropolitan areas, Oklahoma City saw the largest year-over-year increase in rents, one of only two metros, including Pittsburgh, PA, to see increases greater or equal to 20 percent. In total, 13 metros saw year-over-year increases greater than or equal to 10 percent. Another 7 metros saw increases below 10 percent but greater than the national median. Only five metros saw year-over-year price declines.

The following metro areas have experienced the biggest increase in rent prices year-over-year.

- Oklahoma City, OK (+24.1 percent)

- Pittsburgh, PA (+20.0 percent)

- Indianapolis-Carmel-Anderson, IN (+17.9 percent)

- Louisville-Jefferson County, KY-IN (+17.5 percent)

- Nashville-Davidson-Murfreesboro-Franklin, TN (+17 percent)

- Cincinnati, OH-KY-IN (+16.5 percent)

- Raleigh-Cary, NC (+16.4 percent)

- New York-Newark-Jersey City, NY-NJ-PA (+15.4 percent)

- Portland-Vancouver-Hillsboro, OR-WA (+14 percent)

- San Antonio-New Braunfels, TX (+12.5 percent)

The following metro areas have experienced decreases in rent prices year-over-year.

- Milwaukee-Waukesha, WI (-14.3 percent)

- Minneapolis-St. Paul-Bloomington, MN-WI (-8.8 percent)

- Baltimore-Columbia-Towson, MD (-2.8 percent)

- Houston-The Woodlands-Sugar Land, TX (-0.6 percent)

- Chicago-Naperville-Elgin, IL-IN-WI (-0.5 percent)

Rental industry trends

In addition to our pricing trends, here are a few key industry developments.

1. Rents are down but inflation remains high

Rent prices are stabilizing, but don’t expect the consumer price index (CPI) to reflect those changes just yet. Shelter, which includes rents, makes up 30 percent of overall inflation and 40 percent of the core CPI excluding volatile food and energy prices. Consumer inflation rose 8.2 percent in September.

“You’re probably not going to see a lot of slowing in CPI rents,” according to Alan Detmeister, a senior economist at UBS, via Yahoo! Finance. “Most people are on 12-month leases, so it tends to be a relatively slow-moving component and will probably be very elevated for at least the next year.” Analysts collect shelter data for the CPI once every six months and include people with existing leases

But, economists at Goldman Sachs told CNBC that a slowdown in asking rents for new leases combined with a surge in the multifamily constitution and softening rental demand points to a sustained downturn in rent inflation despite current CPI numbers. “We expect shelter inflation to slow to a 0.4-0.5 percent monthly pace by year-end and peak at around 7 percent year-over-year early next year,” the economists said.

2. Homeowners turn to renting their homes instead of selling

Approximately 85 percent of homeowners with mortgage interest rates below five percent are staying put, according to a recent Redfin analysis of the Federal Housing Finance Agency data. Despite high home prices, high-interest rates are discouraging homeowners from moving as it would mean giving up their low rates and potentially taking on larger housing bills. Higher rates have increased the typical monthly mortgage payment by 42 percent from a year ago.

Seller reluctance is one factor contributing to a dearth of new listings, down nearly 20 percent year over year. “The plunge in new listings is hindering growth in housing supply, which is keeping home prices relatively high even though the market is slowing down,” Redfin Deputy Chief Economist Taylor Marr, said. “Housing supply fell 1 percent in August from the month before; normally, it would rise during a downturn.”

The good news, Marr says, is existing homeowners are locked into relatively low rates and many have built hundreds of thousands of dollars in equity during the pandemic-fueled rise in home prices. That means some owners will continue to be enticed by the high selling prices, despite rising rates, especially if considering a move to a more affordable market.

About this report

Our October 2022 Rent Report highlights year-over-year rent trends and price fluctuations that renters may experience in various parts of the United States. We compare rent prices across bedroom types to determine which of the country’s most populated metros are becoming more affordable or more expensive for renters. States and metros with insufficient inventory are excluded from this report.

| CBSA | Population | Median Rent | YoY % Change | MoM % Change |

|---|---|---|---|---|

| Oklahoma City, OK CBSA | 1,441,647 | $1,260 | 24.14% | 1.43% |

| Pittsburgh, PA CBSA | 2,353,538 | $1,923 | 20.02% | -2.04% |

| Indianapolis-Carmel-Anderson, IN CBSA | 2,126,804 | $1,490 | 17.92% | -2.57% |

| Louisville/Jefferson County, KY-IN CBSA | 1,284,566 | $1,412 | 17.52% | -0.89% |

| Nashville-Davidson–Murfreesboro–Franklin, TN CBSA | 2,012,476 | $2,127 | 17.03% | -0.74% |

| Cincinnati, OH-KY-IN CBSA | 2,259,935 | $1,569 | 16.48% | -6.82% |

| Raleigh-Cary, NC CBSA | 1,448,411 | $2,030 | 16.36% | -2.47% |

| New York-Newark-Jersey City, NY-NJ-PA CBSA | 19,768,458 | $4,176 | 15.38% | 0.68% |

| Portland-Vancouver-Hillsboro, OR-WA CBSA | 2,511,612 | $2,602 | 14.00% | -0.50% |

| San Antonio-New Braunfels, TX CBSA | 2,601,788 | $1,418 | 12.54% | -3.27% |

| Buffalo-Cheektowaga, NY CBSA | 1,162,336 | $1,504 | 11.06% | 0.57% |

| New Orleans-Metairie, LA CBSA | 1,261,726 | $1,847 | 11.03% | -2.33% |

| Richmond, VA CBSA | 1,324,062 | $1,798 | 10.38% | 0.01% |

| San Francisco-Oakland-Berkeley, CA CBSA | 4,623,264 | $3,807 | 9.89% | -2.79% |

| Denver-Aurora-Lakewood, CO CBSA | 2,972,566 | $2,752 | 9.73% | 1.65% |

| Detroit-Warren-Dearborn, MI CBSA | 4,365,205 | $1,619 | 9.67% | 3.77% |

| San Diego-Chula Vista-Carlsbad, CA CBSA | 3,286,069 | $3,441 | 9.54% | 0.23% |

| Austin-Round Rock-Georgetown, TX CBSA | 2,352,426 | $2,395 | 8.88% | 1.86% |

| Salt Lake City, UT CBSA | 1,263,061 | $1,921 | 8.86% | -1.94% |

| Dallas-Fort Worth-Arlington, TX CBSA | 7,759,615 | $2,157 | 8.84% | -0.06% |

| Memphis, TN-MS-AR CBSA | 1,336,103 | $1,549 | 7.40% | 0.10% |

| Providence-Warwick, RI-MA CBSA | 1,675,774 | $2,524 | 7.33% | -0.47% |

| Miami-Fort Lauderdale-Pompano Beach, FL CBSA | 6,091,747 | $3,080 | 7.28% | 1.71% |

| Charlotte-Concord-Gastonia, NC-SC CBSA | 2,701,046 | $1,909 | 7.25% | 0.41% |

| Cleveland-Elyria, OH CBSA | 2,075,662 | $1,500 | 6.84% | -1.30% |

| Washington-Arlington-Alexandria, DC-VA-MD-WV CBSA | 6,356,434 | $2,706 | 6.71% | -1.97% |

| Kansas City, MO-KS CBSA | 2,199,490 | $1,528 | 6.63% | 2.86% |

| San Jose-Sunnyvale-Santa Clara, CA CBSA | 1,952,185 | $3,611 | 6.21% | -1.83% |

| Sacramento-Roseville-Folsom, CA CBSA | 2,411,428 | $2,774 | 5.26% | 0.53% |

| Hartford-East Hartford-Middletown, CT CBSA | 1,211,906 | $2,076 | 5.15% | 1.39% |

| Birmingham-Hoover, AL CBSA | 1,114,262 | $1,490 | 4.84% | -2.34% |

| Las Vegas-Henderson-Paradise, NV CBSA | 2,292,476 | $1,878 | 4.80% | 0.03% |

| Philadelphia-Camden-Wilmington, PA-NJ-DE-MD CBSA | 6,228,601 | $2,334 | 4.42% | -2.41% |

| Orlando-Kissimmee-Sanford, FL CBSA | 2,691,925 | $2,121 | 4.24% | -1.51% |

| Tampa-St. Petersburg-Clearwater, FL CBSA | 3,219,514 | $2,173 | 4.11% | -0.46% |

| St. Louis, MO-IL CBSA | 2,809,299 | $1,570 | 4.09% | -1.30% |

| Virginia Beach-Norfolk-Newport News, VA-NC CBSA | 1,803,328 | $1,703 | 3.92% | -1.20% |

| Columbus, OH CBSA | 2,151,017 | $1,558 | 3.16% | -5.73% |

| Seattle-Tacoma-Bellevue, WA CBSA | 4,011,553 | $2,972 | 3.03% | -1.48% |

| Riverside-San Bernardino-Ontario, CA CBSA | 4,653,105 | $2,724 | 2.88% | -0.62% |

| Atlanta-Sandy Springs-Alpharetta, GA CBSA | 6,144,050 | $2,084 | 2.70% | -0.29% |

| Phoenix-Mesa-Chandler, AZ CBSA | 4,946,145 | $2,043 | 1.77% | -0.64% |

| Los Angeles-Long Beach-Anaheim, CA CBSA | 12,997,353 | $3,469 | 1.14% | -3.55% |

| Boston-Cambridge-Newton, MA-NH CBSA | 4,899,932 | $3,731 | 1.12% | -1.46% |

| Jacksonville, FL CBSA | 1,637,666 | $1,649 | 0.21% | 0.89% |

| Chicago-Naperville-Elgin, IL-IN-WI CBSA | 9,509,934 | $2,437 | -0.49% | -0.98% |

| Houston-The Woodlands-Sugar Land, TX CBSA | 7,206,841 | $1,751 | -0.61% | 0.33% |

| Baltimore-Columbia-Towson, MD CBSA | 2,838,327 | $2,041 | -2.84% | -1.93% |

| Minneapolis-St. Paul-Bloomington, MN-WI CBSA | 3,690,512 | $1,735 | -8.81% | 0.16% |

| Milwaukee-Waukesha, WI CBSA | 1,566,487 | $1,633 | -14.29% | 2.46% |

Methodology

We analyzed rental property prices in September 2022, the last full month of data, from Rent.’s available inventory to identify our median rent prices at the national, state and metro levels. Our analysis combines inventory and bedroom types into one simple median that covers all available rental units at the time.

The top 50 metropolitan areas in our analysis are determined by U.S. Census Bureau population estimates for 2021.

More detailed information about our methodology can be found here.

The rent information included in this article is used for illustrative purposes only. The data contained herein do not constitute financial advice or a pricing guarantee for any apartment.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

")

")

")

")

")

{kind=link}