Florida’s college-savings playbook: prepaid vs. the best 529 plans in America

College costs never pause. At Florida public universities, tuition rises about 3–4 percent a year—small bumps that snowball into five-figure jumps.

You have two main ways to fight back: lock in prices with a Florida Prepaid contract, or grow money in a 529 savings plan that covers far more than tuition. Because Florida has no income tax, you can choose any state’s 529—and starting in 2024, roll up to $35,000 of leftover funds into your child’s Roth IRA tax- and penalty-free.

Ahead, we compare both options, rank the top plans, and spotlight one that gifts new parents $50. Ready? Let’s get started.

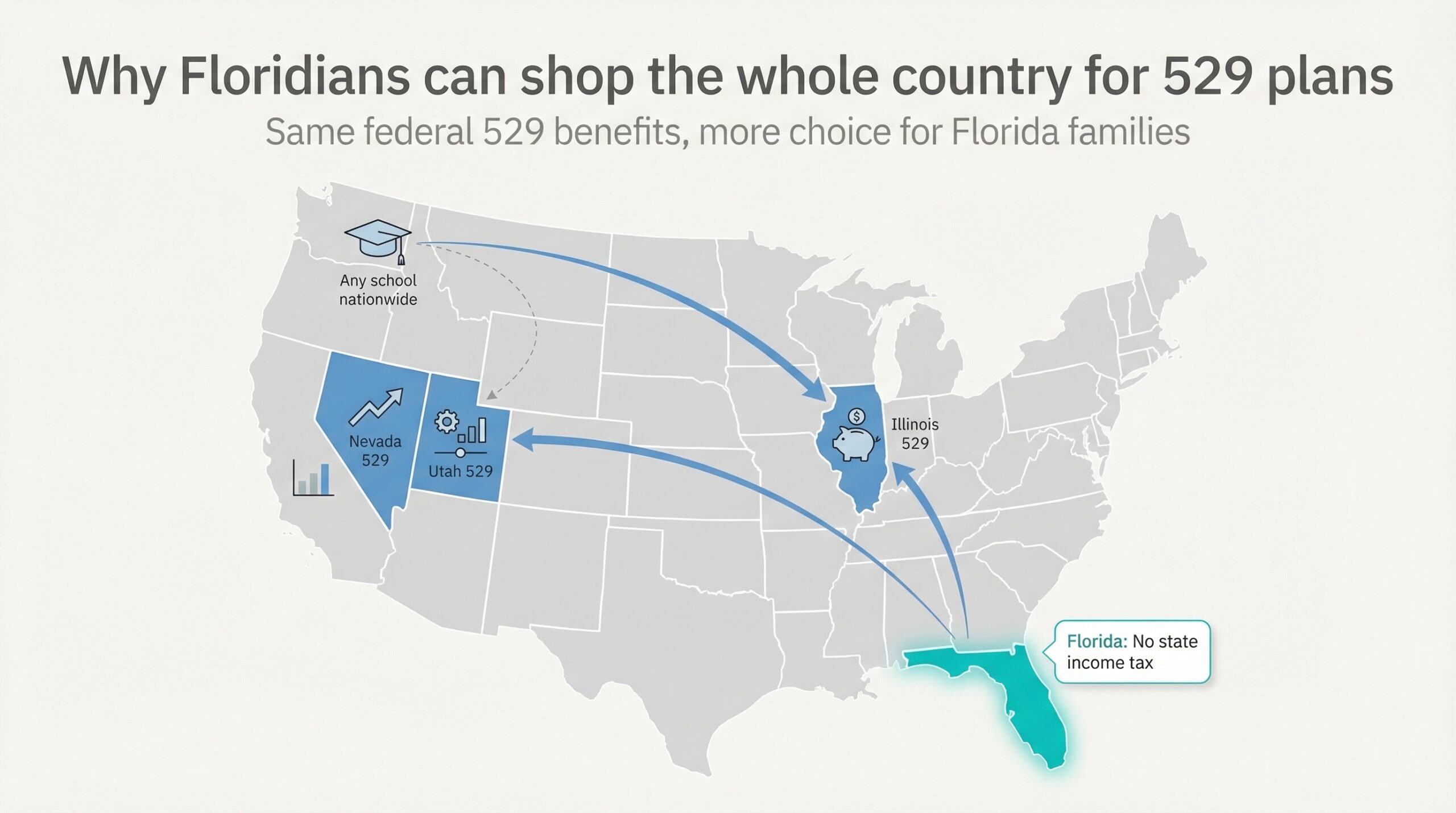

Why Floridians can shop the whole country

Most states offer a tax break that nudges residents toward the home-team 529. Florida doesn’t. With no state income tax, Tallahassee has nothing to deduct and nothing to claw back later.

That single fact turns you into a free agent. A plan in Illinois, Utah, or Nevada provides the same federal tax shelter as Florida’s version: tax-free growth on money used for qualified education costs.

Because everyone starts on equal footing, even tiny fee gaps matter over an 18-year runway. undefined

Portability seals the deal. Any savings-style 529 can pay the bill at the University of Florida, Florida State, or a culinary institute in Oregon. Funds move with the student, not the state seal on the account.

Bottom line: you’re free to pursue the nation’s best-run, lowest-cost plans without giving up a single benefit. Next, we’ll show which ones deserve a Florida parent’s dollars and why.

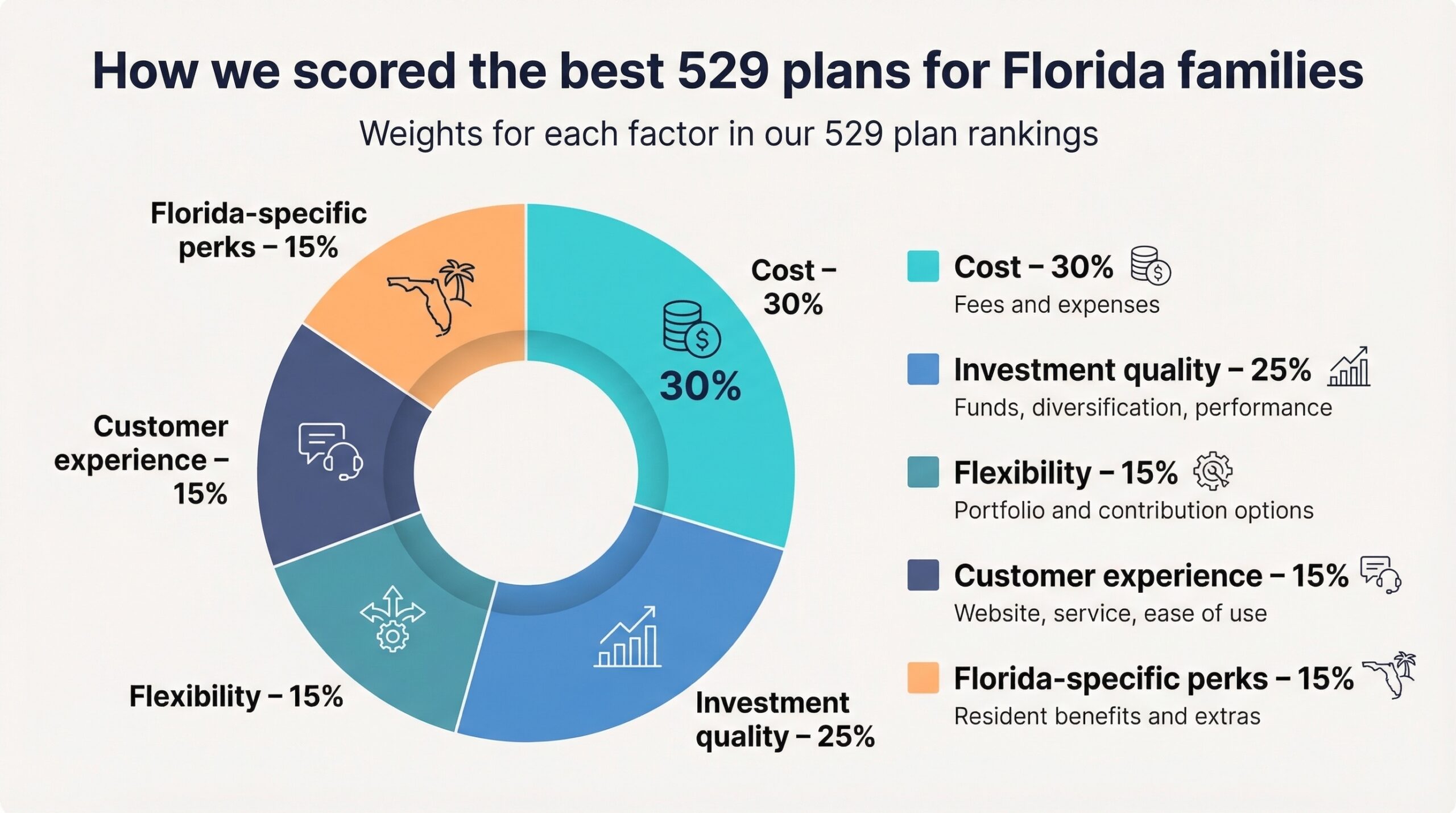

How we picked the winners

Transparency matters. You deserve to know exactly why one plan ranks first while another stays on the bench.

We reviewed every direct-sold 529 savings plan plus Florida Prepaid, a field of more than forty options, and scored each one across five pillars that shape college savings.

Cost carries thirty percent of the grade. Trimming even one basis point from annual fees leaves more money compounding for tuition, so we checked program charges, state surcharges, and underlying fund expenses.

Investment quality counts for twenty-five percent. We looked for broad diversification, sensible age-based glide paths, and trustworthy managers such as Vanguard, Dimensional, and T. Rowe Price. Strong Morningstar ratings and steady results earned extra credit.

Flexibility, customer experience, and Florida-specific perks make up fifteen percent each. Can grandparents gift easily? Does the website invest contributions the same day? Will the plan still look good if you move to Atlanta next year? Practical touches like these separate a good plan from a great one.

After the math, seven programs stood out. You’ll meet them next, starting with the plan that pairs low fees with strong oversight.

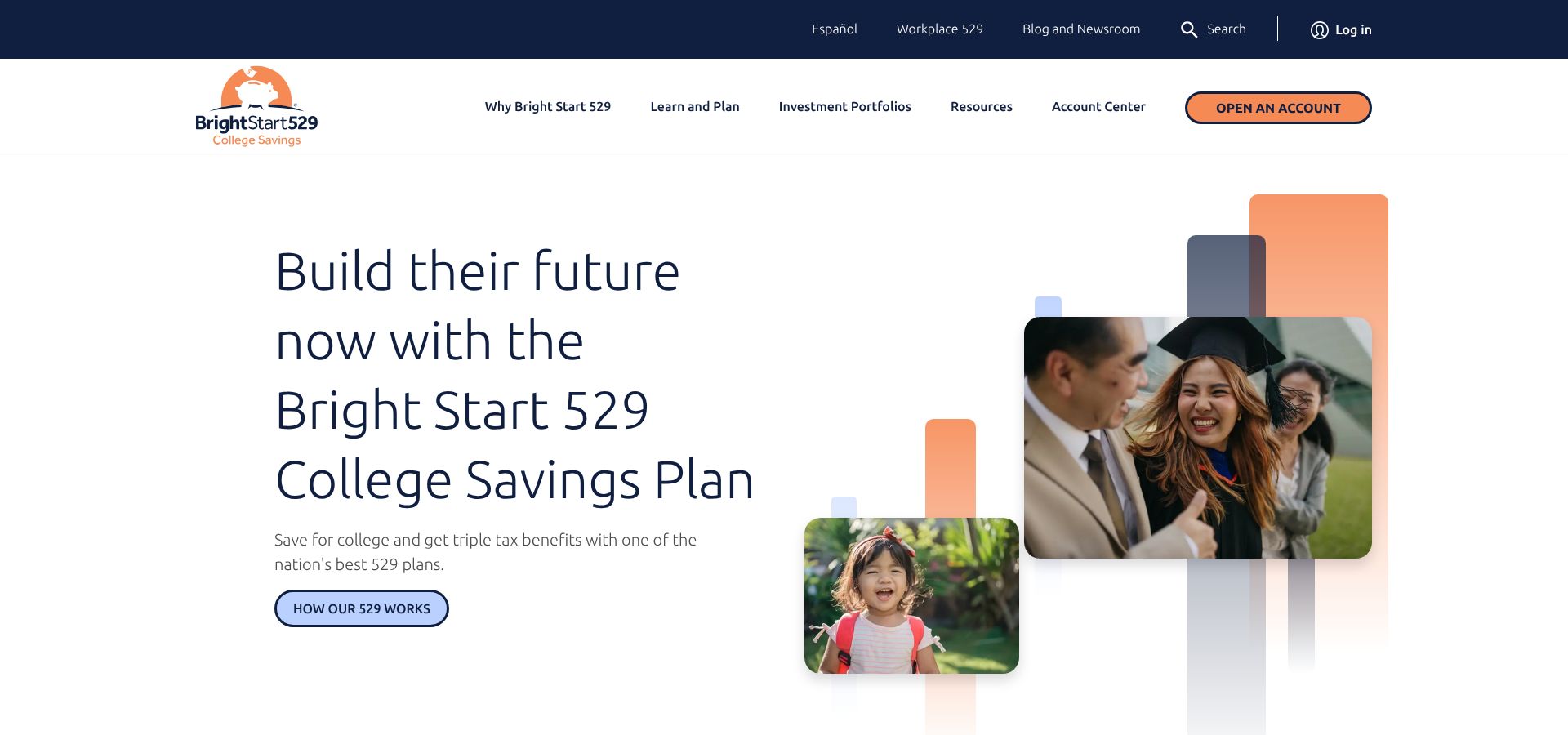

Bright Start (Illinois): our top pick

Bright Start excels at the simplest rule in college saving: lower fees mean more money for tuition.

Bright Start Illinois 529 college savings plan official website screenshot

Morningstar has given the plan its Gold rating for seven consecutive years, citing “exceptional state stewardship and well-constructed portfolios.” That outside endorsement signals elite oversight and results.

Cost matches the praise. The program’s administration fee is 0.10 percent, and many index portfolios sit near 0.13 percent all in after underlying Vanguard and Schwab expenses. On a $25,000 balance, that equates to about thirty dollars a year, a fraction of plans that still charge 0.50 percent.

Choice stays broad. You can coast on an Enrollment Year track that shifts from almost 100 percent stock to a calmer bond mix as college approaches. Prefer some active management? Pick the blend series and let firms such as Dodge & Cox or T. Rowe Price seek extra return. A bank-savings option exists for ultra-conservative dollars.

The website feels current, contributions invest the same business day, and gifting is easy because relatives can send cash through a shareable link rather than a paper check. Illinois adds one more nudge with its First Steps program, which seeds every new Bright Start account opened for a child born or adopted since 2023 with a $50 deposit to help you Kickstart your college savings right out of the gate.

Best for parents seeking maximum growth at low cost who do not mind housing the 529 outside their regular brokerage login. If you like third-party validation, Bright Start supplies plenty.

my529 (Utah): built for tinkerers

If Bright Start is the dependable Honda, Utah’s my529 is the fully loaded Tesla: sleek, low-maintenance, and ready for custom settings.

my529 Utah 529 college savings plan official website screenshot

Morningstar gives it the same Gold medal awarded to Illinois, calling out “an investor-first culture and unrivaled flexibility.” Fees sit near fifteen basis points for the default index age-based portfolio, only a touch higher than Bright Start after Utah’s ninth fee cut in eleven years. Savers pay about fifteen dollars a year on every $10,000 invested, a bargain for do-it-yourself control.

Flexibility leads the pitch. Pick a preset enrollment-year track and let the plan steer, or design your own glide path with up to six funds. Prefer a 90-percent stock mix until eighth grade, then a gradual slide into bonds? You can set that in minutes.

The fund list blends Vanguard index staples with factor-tilted choices from Dimensional Fund Advisors, so value or small-cap fans can seek extra return without leaving the plan.

Website tools feel solid, contributions invest the same business day, and gifting works through a simple link. Utah also accepts payroll direct deposits from many employers.

Best for investors who crave control. If you enjoy fine-tuning allocations or believe in factor investing, my529 hands you the wheel while still keeping total costs low.

Vanguard 529 (Nevada): simple, low cost, and familiar

Sometimes a classic choice feels right. Vanguard’s Nevada plan sticks to the firm’s greatest hits, packages them in a no-frills interface, and prices the bundle near the bottom of the industry.

Costs hover around twelve basis points for the age-based index track, only pennies above Illinois, yet still negligible compared with many state plans. Enrollment and maintenance charges drop to zero when you choose electronic delivery.

Investment choice stays intentionally lean. Three age-based tracks—aggressive, moderate, conservative—plus a handful of static mixes cover every reasonable need. Each relies on Vanguard index funds you likely recognize: Total Stock Market, Total International, and Total Bond. No active bets, no exotic sectors, no urge to outsmart the market.

That simplicity rewards speed and ease. Deposits placed before the market close invest the same day, a perk Florida savers on Bogleheads often praise. Existing Vanguard clients see the 529 alongside IRAs and brokerage accounts, turning rebalancing and cash sweeps into a two-click job.

Gifting is available, though the portal lacks the visual polish of Bright Start. Grandparents still appreciate a straightforward electronic option over mailing a check.

Best for die-hard index investors or anyone who already trusts Vanguard with retirement savings. If you want one login, low fees, and zero decision fatigue, Nevada’s Vanguard plan delivers.

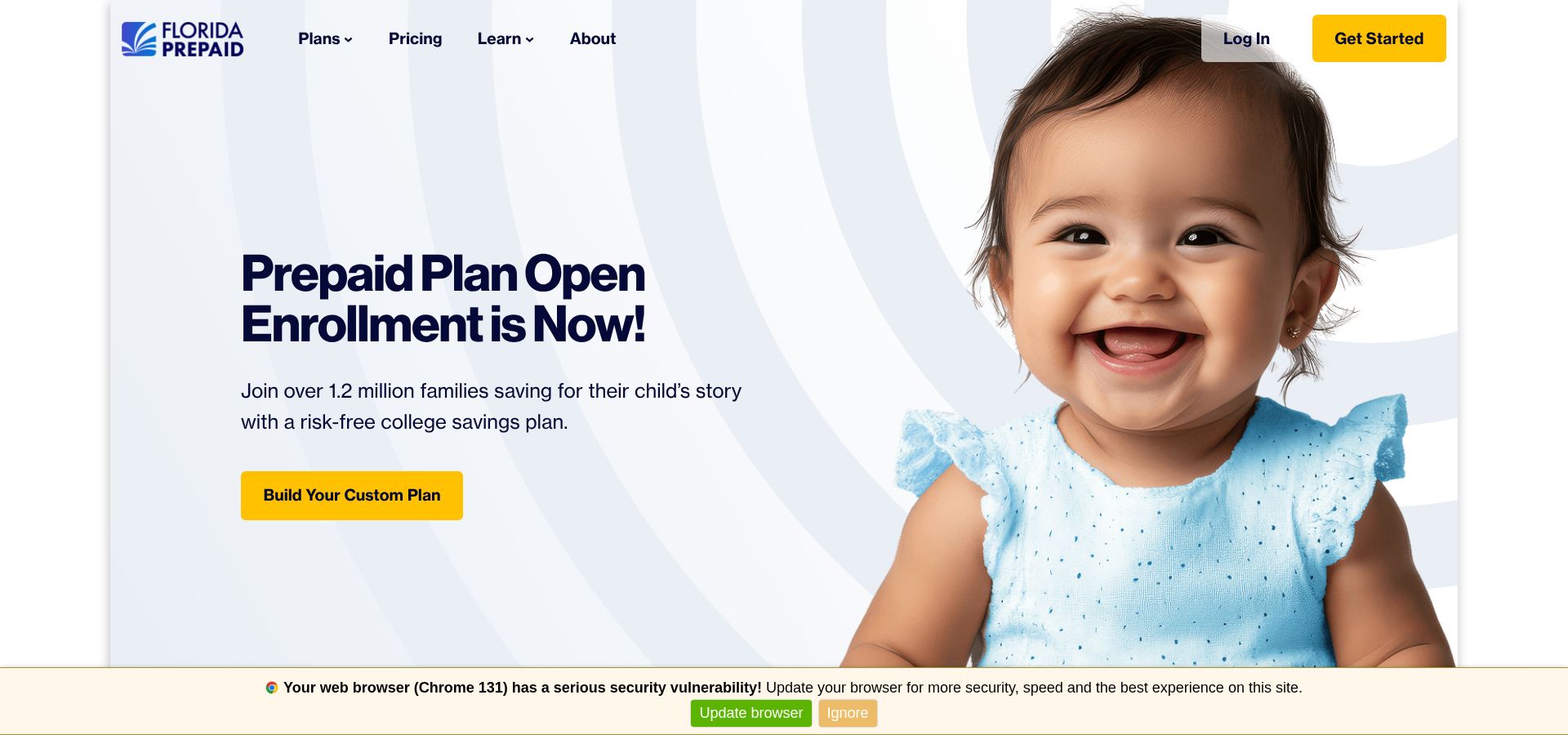

Florida Prepaid College Plan: tuition insurance, Sunshine State style

Picture locking in four years of in-state tuition the way you might reserve a hotel rate months before spring break. That is Florida Prepaid. You pay today’s price, the state guarantees tomorrow’s bill, and market swings become someone else’s problem.

Florida Prepaid College Plan official website screenshot

No annual fees appear on a statement because this is a contract, not an investment account. Your “return” simply tracks tuition inflation. If rates jump, you look smart. If lawmakers freeze tuition, as they did for much of the 2010s, you break even.

Coverage stays narrow: tuition and mandatory fees at Florida public colleges, plus dorm costs if you buy that add-on. Books, meal plans, or a gap year abroad still need separate funding.

Flexibility exists but at a cost. A student can choose an out-of-state or private school, yet the payout caps at the amount Florida would have charged, and you pay the difference. Cancel the contract and you receive your contributions back, often with modest interest, but without the growth a 529 savings plan might deliver.

Who benefits most? Risk-averse families confident their child will attend a Florida public campus. Many parents pair a two-year Prepaid contract with a 529 savings account, securing a safety net while giving extra dollars room to grow.

Bottom line: treat Prepaid as insurance, not an investment. For some households, a guaranteed bill can matter more than chasing market gains.

Florida 529 savings plan: improved, but still playing catch-up

Home-state loyalty has perks, and Florida’s direct-sold 529 earned fresh attention after its 2019 overhaul.

The board removed its program fee, so investors now pay only the costs built into each mutual fund. Stick with Vanguard or BlackRock index options and your all-in expense ratio can sit near twenty basis points—solid, yet still higher than the cheapest national plans.

Menu depth looks strong: twenty age-based Enrollment Year portfolios that rebalance quarterly, six static mixes, and fifteen single-fund choices ranging from Vanguard index funds to Dimensional factor strategies. On paper, you can build a portfolio as sophisticated as Utah’s.

Execution is where Florida trails. Users report two-day delays before contributions reach the market and a portal that feels stuck in 2012. Those hiccups eat into fee savings and add friction parents do not face with Bright Start or Vanguard.

Residency rules also tightened. Either the account owner or the child must live in Florida at opening, and adding money may grow tricky if the family later moves.

Best for Floridians who want an in-state option and can tolerate an older website in exchange for reasonable costs and many fund choices. If you already hold a Florida 529, staying put makes sense. Starting fresh? National leaders still hold the edge.

How the top plans stack up

Numbers tell the story faster than any sales pitch. The grid below highlights the metrics that separate our Florida-friendly front-runners. Focus on the fee column first; every basis point saved is money your student keeps.

![]()

| Plan | Type | Typical all-in fee | Investment highlights | Morningstar rating* | Ideal for |

| Bright Start (IL) | 529 savings | ≈ 0.13% | Index and active tracks, solid glide path | Gold | Lowest cost, quick growth |

| my529 (UT) | 529 savings | ≈ 0.15% | Custom portfolios, DFA factor funds | Gold | DIY investors, tinkerers |

| Vanguard / NV | 529 savings | ≈ 0.12% | Pure Vanguard index funds | Silver | One-login simplicity |

| Florida Prepaid | Prepaid tuition | N/A (contract price) | Guarantees FL public tuition | Not rated | Risk-averse, in-state certainty |

| Florida 529 | 529 savings | ≈ 0.20% (index track) | 20 enrollment-year options | Bronze | Stay-local savers |

| Fidelity (MA/NH) | 529 savings | ≈ 0.15% | Fidelity index and active mix | Gold / Silver | Fidelity loyalists |

*Morningstar 2025 medals for direct-sold versions.

Frequently asked questions

Conclusion

Use this grid as a quick gut check. Plans that combine a Gold rating with fees below 0.15 percent sit in the top tier. Anything costlier deserves extra scrutiny before you click Open account.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

")

{kind=link}