Do you have enough money saved to weather an unexpected job loss? If you are an adult in the U.S., your answer is likely no.

More than two-thirds of Americans — 68 percent — say they’re worried they wouldn’t be able to cover their living expenses for just one month if they lost their primary source of income tomorrow, according to a recent Bankrate survey.

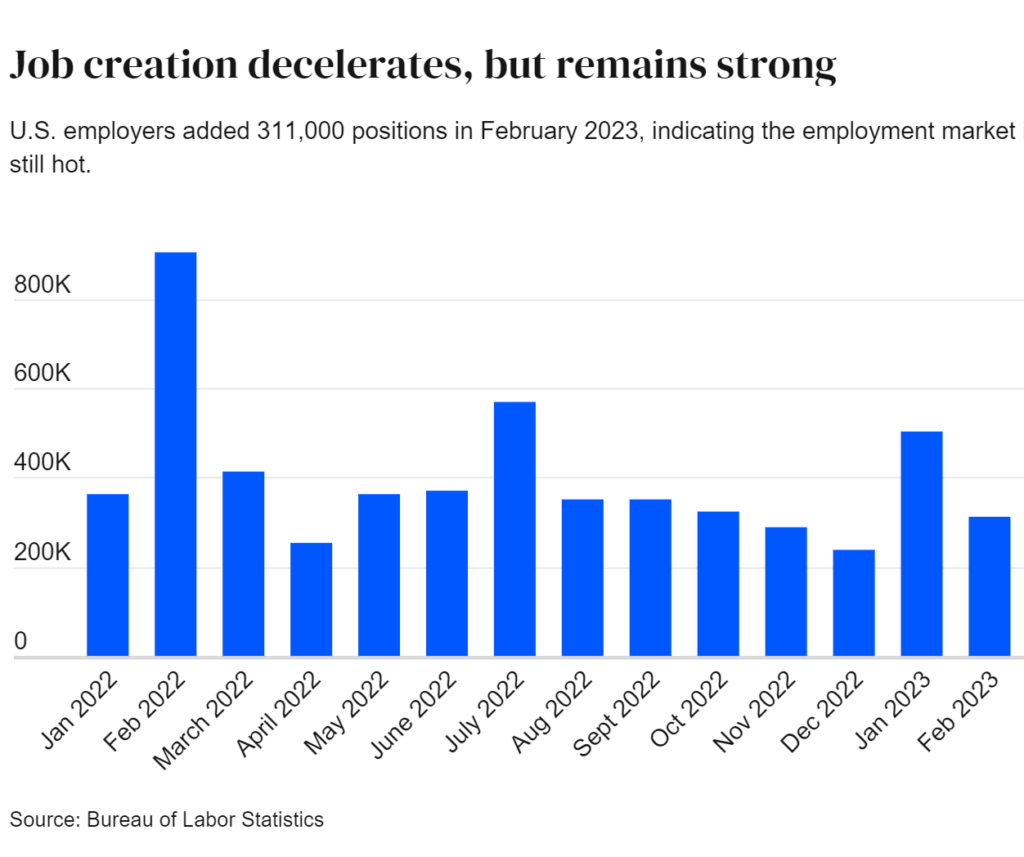

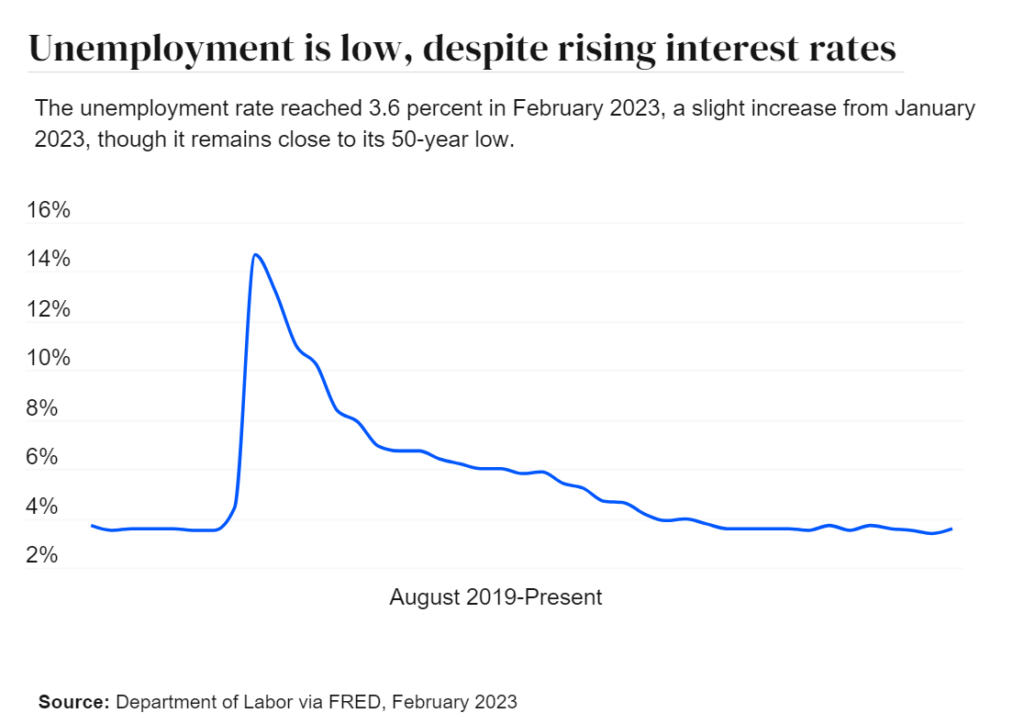

The finding comes when the job market is still punching above its weight. Employers added 311,000 jobs to the U.S. economy in February, and the unemployment rate ticked up slightly to 3.6 percent from 3.4 percent — still an exceptionally low level. Inflation has been slowly coming down in recent months, too.

But the hot job market could cool significantly this year amid the Federal Reserve’s inflation-fighting campaign. The Fed predicts unemployment to rise to 4.6 percent by the end of 2023 as it continues to raise interest rates to rein in stubborn inflation. That means about 7.78 million people would be out of a job, accounting for population growth, says Bankrate’s economic analyst Sarah Foster.

If the economy stalls and unemployment increases, many Americans — especially those with little or no savings — could face financial hardship. One way Americans can prepare for that is “to essentially take out a measure of ‘self-insurance’ by prioritizing emergency savings,” according to Mark Hamrick, Bankrate’s senior economic analyst.

“Some of the best financial practices are advisable during good times as well as not-so-good,” he said. “I’d put emergency savings, saving for retirement and paying down or paying off debt at the top of the ‘to-do’ list.”

Key takeaways about the job market and emergency savings

- Half of Americans are struggling to save, despite the strong job market. Forty-nine percent of Americans have less or no savings than a year ago. And only 43 percent said they could cover an emergency of $1,000 or more using funds from their savings account.

- Most Americans are worried about having enough savings to weather unemployment. Sixty-eight percent of U.S. adults are worried they wouldn’t be able to cover their living expenses for just one month if they lost their primary source of income tomorrow.

- Inflation and unemployment are to blame for fewer savings. Sixty-eight percent are saving less due to inflation (up from 49 percent last year). Forty-four percent of Americans say income or employment status change is causing them to save less for unexpected expenses.

- The hot job market will likely cool later this year. Unemployment is expected to rise to 4.6 percent by the end of 2023, according to a December 2022 Fed forecast.

The job market is healthy, but recession fears are still lingering

The U.S. economy is throwing everyone for a loop. Inflation has been cooling, but not fast enough for the Fed’s liking. Interest rates are rising, and consumers keep spending. And while layoffs in the tech sector have alarmed workers, unemployment remains historically low.

The resilient economy hasn’t stopped some economists from forecasting a recession, though. Economists surveyed by Bankrate at the end of 2022 put the odds of a 2023 recession at 64 percent, but two experts (or 15 percent) said the financial system could avoid a downturn altogether. Bankrate’s fourth-quarter forecast of a recession over the next 12 months also went up significantly from just 33 percent in the first-quarter poll to 52 percent in the second quarter.

For now, the labor market remains remarkably strong and resilient. Job creation decelerated in February but was still stronger than economists expected. Certain industries, like leisure and hospitality, are powering the labor market right now because employers are trying to meet increased demand after the pandemic and recover pandemic-era job losses. Leisure and hospitality added 105,000 jobs in February, though that sector remained 2.4 percent below its level three years ago. Retail, construction and health care also saw gains in February.

“The job market was dealt an almost unprecedented blow by the pandemic when 22 million jobs were lost in two months,” Hamrick said. “The effort to recover from that while also accommodating innovation and new demand has been ongoing ever since.”

“The job market was dealt an almost unprecedented blow by the pandemic when 22 million jobs were lost in two months,” Hamrick said. “The effort to recover from that while also accommodating innovation and new demand has been ongoing ever since.”

Here’s what the economic data says so far about the job outlook in 2023.

Unemployment is historically low, but it’s lasting longer for some Americans

The labor market is off to a better-than-expected start in 2023. The unemployment rate, an indicator of the strength of the job market, rose to 3.6 percent in February. Though the jobless rate increased from January, it’s still near the lowest level in over 50 years.

Unemployment is low, and people are also spending less time in it. The median duration of unemployment fell to 8.3 weeks in February, according to Federal Reserve Economic Data (FRED).

Unemployment is low, and people are also spending less time in it. The median duration of unemployment fell to 8.3 weeks in February, according to Federal Reserve Economic Data (FRED).

But some Americans may be starting to spend longer looking for jobs. Labor Department data shows 805,000 Americans were unemployed for 15 to 26 weeks in February, up from 526,000 people who were unemployed for the same duration in April 2022. Though the duration of people unemployed for 15-26 weeks has ticked up since April, it’s fallen for those who’ve been jobless for 27 weeks or longer over the same period.

Layoffs are low, despite Big Tech

When the economy slows down, companies typically respond by laying off workers. With the exception of some high-profile companies, mainly in the tech sector, there’s little evidence of widespread job cuts.

The layoff rate rose to a still-low 1.1 percent in January 2023 from 1.0 percent in December 2022, well below its pre-pandemic peak of 1.3 percent, according to Job Openings and Labor Turnover Survey data. Filings for unemployment insurance have hardly risen in recent months.

“The job market has remained remarkably resilient even amid increasing numbers of layoffs and job cut announcements,” Hamrick said.

Hiring is slowing down

Hiring is still relatively strong but has been showing signs of cooling. The hiring rate and number of new hires cooled in the second half of 2022, though there are still a lot of jobs available. Hamrick said the mismatch between available jobs and workers is something that Fed Chair Jerome Powell has repeatedly expressed concern about, as it could continue to put upward pressure on wages and keep inflation elevated. Wage growth over the last three months slowed to just 3.6 percent.

Despite job market resilience, Americans are struggling to save

The question on everyone’s mind is whether today’s job market will stay resilient. Experts say that if the economy continues to slow, the job market will eventually follow suit.

“The strength in the labor market gives the Fed the leeway to raise rates more,” said Kayla Bruun, an economic analyst at Morning Consult. “That’s going to hurt employment. We just don’t know quite how much and when.”

At the same time, Americans are struggling to save. A Bankrate survey in January found nearly half of Americans have less or no savings compared to a year ago (49 percent). And only 43 percent said they could cover an emergency of $1,000 or more using funds from their savings account. A quarter would pay for an unexpected $1,000 expense using a credit card while paying it off over time — the largest percentage since Bankrate began collecting data on emergency savings in 2014. Consumers’ personal savings rate is 4.7 percent as of January, up slightly compared to previous months.

Recent Bankrate data shows that inflation is the primary economic reason Americans are struggling to save. Sixty-eight percent of people are saving less due to inflation or rising prices — up from 49 percent last year — followed by rising interest rates (48 percent) and change in income or employment status (44 percent).

“It would be hard to see savings making a strong rebound,” Bruun said.

The possibility of losing a primary source of income has Americans on edge

If put in an income pinch, most Americans would experience heightened anxiety over whether they have enough emergency savings to keep them afloat.

More than 2 in 3 Americans (68 percent) would be worried about having enough emergency savings to cover a month’s worth of living expenses — including 45 percent who would be very worried. Only 14 percent of people would not at all be worried.

Historically disadvantaged groups would feel even more financially vulnerable in the event of income loss, according to Bankrate data.

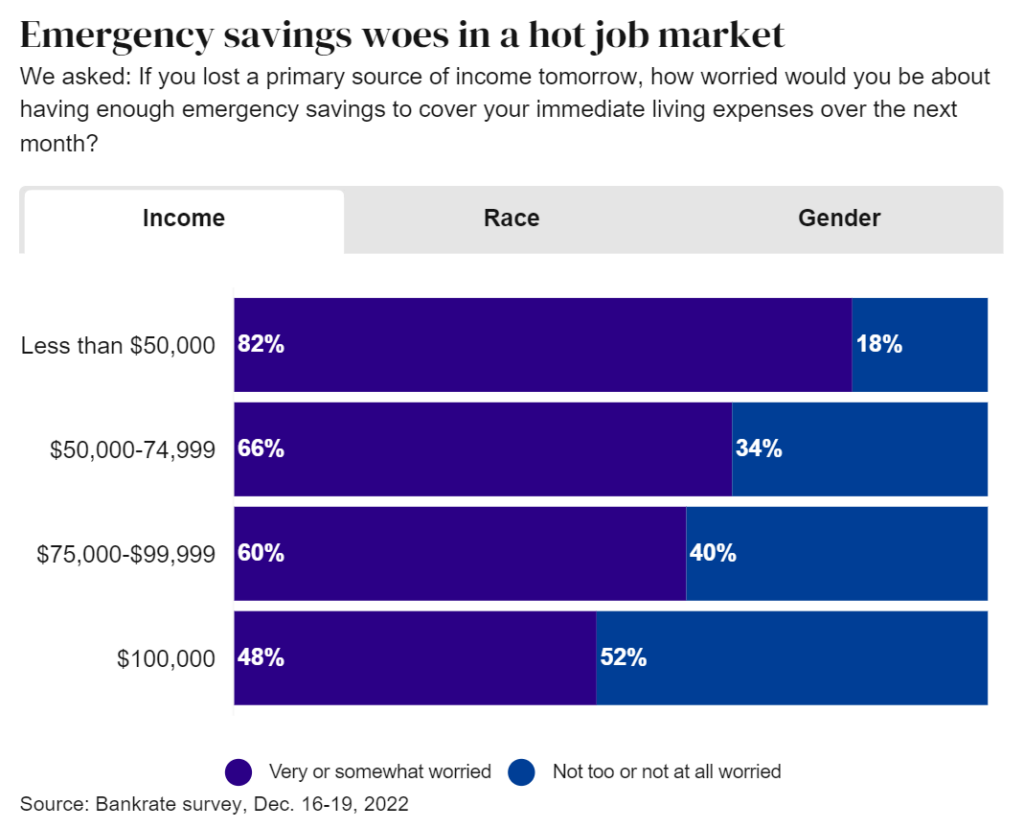

A significant portion of those with lower incomes are more likely to worry about covering a month’s worth of expenses if they lost their income — 82 percent of households earning less than $50,000 would be concerned, compared to 66 percent of middle-income households (between $50,000 and $74,999), 60 percent of upper middle-income households (between $75,000 and $99,999) and 48 percent of high-income households ($100,000+).

A significant portion of those with lower incomes are more likely to worry about covering a month’s worth of expenses if they lost their income — 82 percent of households earning less than $50,000 would be concerned, compared to 66 percent of middle-income households (between $50,000 and $74,999), 60 percent of upper middle-income households (between $75,000 and $99,999) and 48 percent of high-income households ($100,000+).

People of color are also more likely to be stressed about affording a month of living expenses if faced with unemployment. Sixty-three percent of Hispanic Americans and 54 percent of Black Americans said they were very worried, compared to only 39 percent of White Americans.

Additionally, women are much more likely to worry about being able to afford a month of living expenses (72 percent) if they lose their primary income, compared to men (64 percent).

3 ways to boost your emergency savings

An emergency fund can be a lifeline if you experience a sudden loss of income or an extended period of unemployment. With unemployment expected to rise later this year, it’s even more critical to ensure you have enough savings set aside for the unexpected. These are three simple ways to give your savings that extra boost:

1. Start small and make it a habit

Financial experts usually recommend saving three to six months’ worth of expenses, but if more prolonged periods of unemployment become more common, it may make sense to put away even more. Putting away what you can — even if it’s just a few dollars a day — can make a difference over time, says Nilay Gandhi, CFP and senior wealth advisor at Vanguard.

“Aim to save 12 to 14 percent of your paycheck, whether that ends up going into a retirement plan, a Roth IRA, or even emergency savings,” Gandhi said. “But even 1 percent is better than nothing.”

Automating the process is an effective way to turn saving into a long-term habit. Set up a direct deposit to redirect part of your paycheck into a savings account, ideally in a high-yield savings account that rewards you for saving.

2. Revisit your budget and trim where you can

Now is an ideal time to scrutinize your budget and make it as lean as possible. Look where you can cut nonessential expenses — like vacations or subscriptions — and right-size your household budget to avoid plummeting into stress spirals.

If you’re struggling to trim or adjust your budget, it may help to think about where you want your budget to be in a worst-case scenario. Ask yourself what expenses you’re willing to cut back on if you lost your job or had an expensive medical emergency.

3. Look for additional streams of income

If your budget feels tighter than usual or you want to boost your savings, consider branching out and finding additional income streams.

Building a side hustle, freelancing, or working a part-time job could all add extra cushion to your budget or accelerate your ability to achieve financial independence. It can also support you with extra money when unexpected work circumstances arise.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

")

")

{kind=link}