By Telis Demos

More Americans than ever will turn 65 in 2025. That will be a dominant theme for financial stocks in the years ahead.

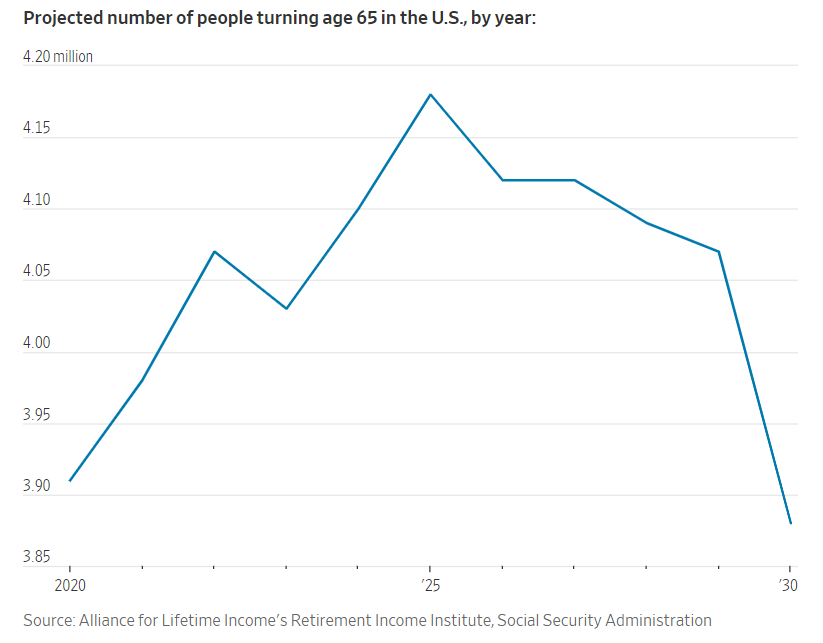

About 4.2 million people in the U.S. are forecast to cross that age threshold next year, according to a report by the Alliance for Lifetime Income’s Retirement Income Institute, citing Social Security Administration figures. This could represent the height of what is termed the “peak 65” zone, a period of years from 2024 to 2027 in which more than 4.1 million will hit that age level each year.

For financial services firms, that likely means more demand for investments that can help people close the income gap they expect from not working. That can be as simple as putting their cash into higher-yielding vehicles, such as money-market funds. Already, investors’ close attention to cash yields is a challenge for banks and brokers accustomed to supercheap deposits.

They are growing fast. Back in 2022, U.S. individual retail annuity sales were less than $300 billion, according to Wink, a life insurance market research firm. Sales are expected to be around $450 billion in 2024 and are forecast to exceed $520 billion in 2025.

“As long as rates remain attractive and the market is on the upswing, annuity sales will flourish,” says Wink Chief Executive Sheryl Moore. “The ‘silver tsunami’ is embracing annuities in a way we’ve never seen before.”

One thing to watch will be whether more companies begin to add annuity options to their defined-contribution retirement plans which, unlike traditional pensions, don’t necessarily guarantee any income.

The likes of BlackRock and JPMorgan Chase’s asset-management arm are offering products akin to target-date funds with embedded annuities, though adoption hasn’t yet been widespread by companies that sponsor retirement plans. More annuity growth could also help further fuel revenue expansion for insurers who sell annuities or backstop annuity risks, such as publicly traded Brighthouse Financial, Equitable, Prudential and others.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

{kind=link}