If you’re not living in the best place to retire, you probably know it by now. Just look at your bank account.

The price you pay in your community for groceries, gasoline, housing and other essentials will significantly impact your quality of life. And if you’re having trouble affording them now, imagine doing it while retired on a fixed income.

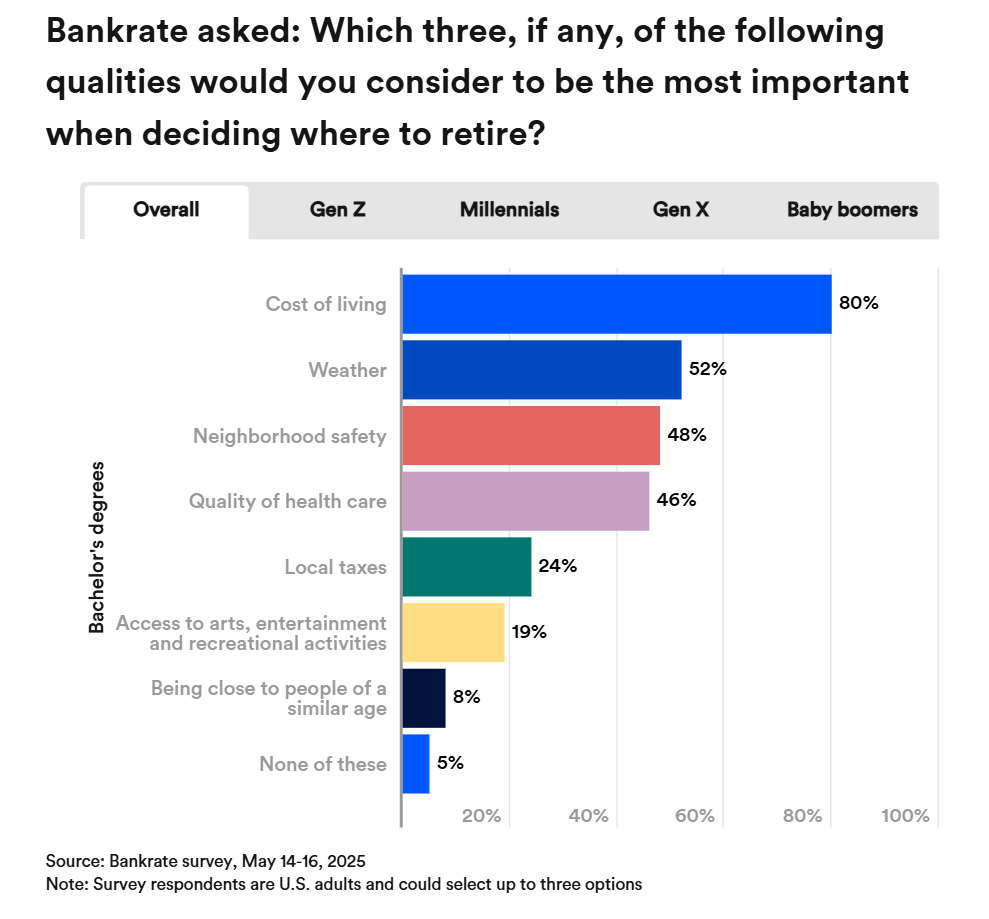

Americans, in fact, value a community’s cost of living more than just about anything else, according to a recent Bankrate public opinion survey. Eight in 10 said it would be a top concern when deciding where to retire.

Affordability was cited much more often in the survey than other qualities typically associated with retirement such as sunny skies, no-shovel winters, top-flight healthcare and safe streets. The survey also found that people appear to become increasingly sensitive to the cost of living the closer they get to retirement and the less disposable income they have to throw around.

Eighty-four percent of Gen Xers and 83 percent of baby boomers said cost of living is their biggest concern, compared with 74 percent of Gen Zers and 78 percent of millennials. And 85 percent of Americans earning under $50,000 ranked affordability as their top factor, compared with 74 percent of those making over $100,000.

In some cases, affordability can be improved by downsizing your home or trimming your budget. But many Americans have opted for another method: moving to a cheaper location.

If you can sell your place, downsize to an area with a lower cost of living and pay cash, that might make it a great move for you. — Kerry HannonAuthor of “Retirement Bites”

A median-priced home costs roughly $200,000 less in Florida than it does in New York, for example. If you move from Boston to Charleston, South Carolina, you’ll save about 25 cents per gallon on gasoline, at least $4 every time you grocery shop and over $100 on your electricity bill.

But, as many retirees find out, a cheaper location isn’t always better. Some low-cost states also have the worst healthcare systems, the highest crime rates, more natural disasters. Younger boomers and Gen Xers, Hannon added, are especially aware that traditional retirement destinations — like Florida and Arizona — may no longer be the bargain they once were and introduce other risks.

“It just became sort of ingrained that those were logical places because you didn’t have to deal with inclement weather,” Hannon said. “They’re [Gen Xers and younger baby boomers] more cognizant of the fact that the whole thing has been upended to a certain degree.”

Retirees in the next generation are likely to consider a variety of factors before choosing where to spend their golden years. Besides affordability, the survey found that 52 percent ranked weather as a top priority and 48 percent said the same of neighborhood safety. Survey respondents could pick up to three qualities as most important.

6 important considerations for a retirement spot

Considering a retirement move? With inflation eroding buying power and health costs climbing, experts say Americans approaching retirement are weighing trade-offs more carefully than ever.

In addition to affordability, here are six other factors you should weigh when deciding where to settle down, according to retirement experts.

1. Your retirement savings

Before you relocate for retirement, make sure your finances line up. Here are some steps that Collinson and Hannon recommend:

- Know your budget. Track your spending habits so you understand what you can actually afford.

- Figure out your income streams. Add up Social Security, retirement savings and other assets (like home equity) to see how long they’ll last.

- Think about timing Social Security. You can claim at 62, but waiting means bigger checks for life. Benefits grow about 8 percent every year you delay past full retirement age until 70.

- Be realistic about retirement age. Many people stop working at 62 or 63, the median age of retirement, which means fewer years of earnings and more years to cover with savings, according to Collinson.

- Run the numbers. Use Bankrate’s retirement calculator or the “25x rule” (annual income needed × 25) as a quick gut check.

- Use free resources. Your 401(k) or retirement plan provider likely offers free planning tools. Take advantage of them while you have access.

- Consider professional help. A financial advisor can give you personalized guidance and a solid plan.

“ We’ve seen high rates of inflation in past years, which erodes our buying power, so affordability is just that much more important. People are feeling a squeeze, whether they’re in the workforce or retired.” — Catherine Collinson, CEO of Transamerica Center for Retirement Studies

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

")

{kind=link}