Consumers are increasingly relying on credit cards to make ends meet, but their credit rating hasn’t suffered.

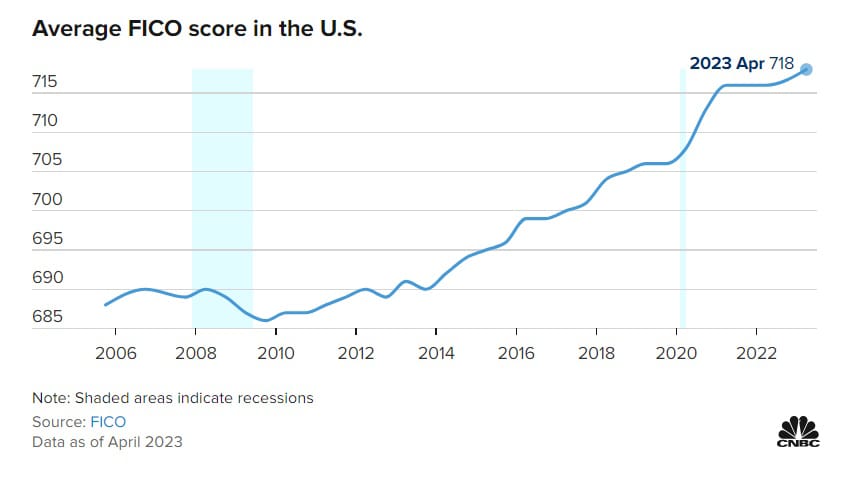

Even as credit card balances for Americans surpassed $1 trillion for the first time ever, the national average credit score rose two points from a year ago to reach a new high of 718, according to a report from FICO, developer of one of the scores most widely used by lenders. FICO scores range between 300 and 850.

Credit scores rose as consumers took on more debt

As higher prices weighed on most Americans’ financial standing, consumers, as a whole, have fallen deeper in debt, causing an increase in credit card balances and an uptick in missed payments.

As of April, the average credit card utilization was 34%, up from 31% a year earlier.

Your utilization rate, the ratio of debt to total credit, is one of the factors that can influence your score. Credit experts generally advise borrowers to keep revolving debt below 30% of their available credit to limit the effect that high balances can have.

Still, delinquency rates are low by historical standards, said Ted Rossman, senior industry analyst at Bankrate. “People are working and keeping up with their bills.

Still, delinquency rates are low by historical standards, said Ted Rossman, senior industry analyst at Bankrate. “People are working and keeping up with their bills.

“Even if they are not saving more, they are keeping up, for the most part.”

A strong labor market and cooling inflation have helped offset high interest rates and consumer prices, FICO found, and so has the removal of certain medical collections data from consumer credit files.

Experts also expect the resumption of student loan payments to take a bite out of household budgets, while elevated gas prices and geopolitical tensions are hitting confidence levels.

What is a ‘good’ credit score?

Generally speaking, the higher your credit score, the better off you are when it comes to getting a loan. You’re more likely to be approved, and if you’re approved, you can qualify for a lower interest rate.

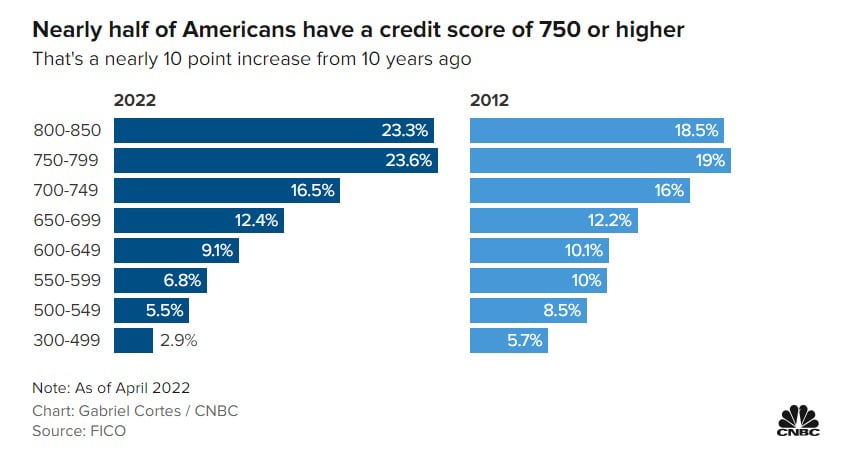

A good score generally is above 670, a very good score is over 740 and anything above 800 is considered exceptional.

An average score of 718 by FICO measurements means most lenders will consider your creditworthiness “good” and are more likely to extend lower rates.

An average score of 718 by FICO measurements means most lenders will consider your creditworthiness “good” and are more likely to extend lower rates.

Average nationwide credit scores bottomed out at 686 during the housing crisis more than a decade ago, when there was a sharp increase in foreclosures. They steadily ticked higher until the Covid-19 pandemic, when government stimulus programs and a spike in household saving helped scores jump to a historical high.

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

Landscape")

{kind=link}