The global financial landscape is confronting a structural anomaly: a highly capitalized tier of super-unicorns whose private valuations and infrastructure footprints dwarf those of typical public entities at listing. For nearly a decade, abundant late-stage venture capital and secondary markets allowed hyper-growth companies to delay initial public offerings (IPOs). However, shifting macroeconomic realities, institutional liquidity demands, and the sheer scale of capital required to fund frontier technologies have brought the private market paradigm to a critical crossroad.

The impending transition of pioneering firms like SpaceX and OpenAI into the public market pipeline represents a fundamental evolution in market architecture. These companies are no longer viewed merely as fast-growing technology startups; they operate as geopolitical chess pieces, global telecommunications backbones, and foundational computational infrastructures. Consequently, preparing for a public filing in this landscape requires far more than standard regulatory paperwork—it demands deep structural realignments, corporate governance transformations, and the navigation of complex regulatory barriers.

The Super-Unicorn Landscape

To understand the magnitude of the upcoming IPO pipeline, it is essential to map the valuations and core structural drivers behind the most anticipated public filings.

| Corporation | Target Sector | Primary IPO Catalyst | Governance Hurdles |

| SpaceX (Starlink) | Aerospace & Satellite Telecom | Global commercial monetization; sovereign enterprise contracts | Multi-class share structures; national security asset oversight |

| OpenAI | Artificial Intelligence Infrastructure | Massive compute scaling costs; transition away from capped-profit models | Non-profit board control liquidation; public asset distribution |

| Stripe | Global Financial Rails & Payments | Mature cross-border revenue; employee equity and RSU expiration dates | Regional compliance; macroeconomic transaction-volume shifts |

| Databricks | Data Engineering & Cloud Software | Enterprise data lakehouse dominance; clean liquidity path amid M&A blocks | Competitive cloud pricing; AI data integration scaling |

SpaceX and the Starlink Spin-Off Mechanics

SpaceX has historically resisted the traditional public market path for its core aerospace operations. The company’s primary mission—establishing multi-planetary life through the development of the Starship launch vehicle—requires high-risk, capital-intensive R&D cycles that don’t align with the short-term, quarter-by-quarter scrutiny of public equity markets. However, its low-Earth orbit (LEO) satellite internet subsidiary, Starlink, represents an entirely different economic asset.

Starlink has rapidly matured from a speculative constellation project into a cash-generative powerhouse with immense global utility. The entity has evolved into a strategic sovereign asset, as demonstrated by continuous high-level international negotiations. For instance, European nations like Italy have engaged in explicit regulatory and legislative discussions to integrate Starlink technology directly into state telecommunications architectures to satisfy digital sovereignism initiatives.

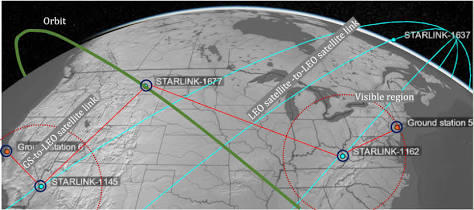

As illustrated in the constellation architecture schematic, Starlink relies on a complex network of satellite-to-satellite laser crosslinks, ground stations, and dynamic orbital pathways to provide ultra-low latency data routing across the globe. This architectural layout allows Starlink to bypass traditional terrestrial fiber limitations, capturing lucrative enterprise markets in maritime shipping, defense communications, commercial aviation, and remote regional infrastructure.

Because Starlink operates a highly predictable, recurring subscription model that can safely self-fund its operational scaling, financial institutions view it as the ideal candidate for a public tracking stock or an isolated corporate spin-off. A targeted public listing would allow public markets to cleanly value Starlink’s utility mechanics while insulating SpaceX’s deep-space exploratory programs from public equity volatility.

OpenAI’s Structural Realignment for Public Markets

While SpaceX navigates structural decisions based on capital allocation, OpenAI’s path toward a public filing requires a complete corporate re-engineering. OpenAI was founded as a non-profit organization, later adopting an “Aligned Structuring” design that placed a capped-profit commercial arm under the absolute control of a non-profit board. This structure was legally designed to prioritize public safety and ethical AI deployment over profit maximization.

However, the economics of frontier AI development have broken the boundaries of traditional venture-backed structures. The initial phase of the foundation model era—characterized by simple pre-training scaling laws—has transformed into a hyper-competitive race where frontier training runs demand billions of dollars in hardware, energy, and localized data infrastructure. With inference costs plummeting and open-weight models matching early proprietary moats, sustaining a competitive advantage requires permanent capital pools that only public equity markets can sustain.

Corporate Law Transition: Capped-profit frameworks are fundamentally incompatible with public equity markets. Public institutional investors cannot easily underwrite, trade, or value shares that possess hard limits on financial returns or are subordinate to a non-profit board’s unilateral decision-making.

Consequently, OpenAI has initiated structural overhauls to transition into a standard, commercial for-profit entity. This transition involves dissolving legacy return caps and restructuring equity agreements to satisfy public regulatory standards. This corporate re-engineering is a necessary precursor to an IPO, allowing public markets to evaluate the firm under standard fiduciary duties and clear corporate governance laws.

The Enterprise Heavyweights: Stripe and Databricks

While deep-tech and AI architectures dominate public interest, mature enterprise giants like Stripe and Databricks represent the traditional foundation of the upcoming IPO pipeline. These companies have achieved massive scale, solid unit economics, and predictable revenue models, yet they face distinct private-market exit pressures.

Stripe and the RSU Liquidity Mandate

Stripe stands as a principal pillar of platform capitalism, processing hundreds of billions in cross-border digital transactions annually. For a company of Stripe’s maturity, the primary driver for an initial public offering is no longer early-stage growth capital, but rather the structural reality of employee compensation.

Silicon Valley enterprises heavily utilize Restricted Stock Units (RSUs) with explicit 10-year expiration horizons. As a company approaches a decade as a highly valued private entity, early employee and executive stock grants risk expiring, creating substantial tax complexities and liquidity strains. While Stripe has previously executed large-scale private secondary sales to alleviate these pressures, a formal public listing remains the most efficient, permanent mechanism to clear mature equity overhangs and satisfy institutional liquidity mandates.

Databricks and the Regulatory M&A Bottleneck

Databricks has established dominant positioning in enterprise data management through its pioneering “data lakehouse” architecture—a unified system combining the raw storage capacity of data lakes with the structured transactional capabilities of traditional databases. The company enjoys robust, sticky enterprise revenue, making it structurally public-ready.

The catalyst driving Databricks toward a clean public listing is heavily reinforced by a tightening regulatory environment. Antitrust enforcement agencies have placed immense scrutiny on technology consolidation, practically eliminating the possibility of strategic buyouts for mega-unicorns. Regulatory frameworks like the Hart-Scott-Rodino (HSR) Act are actively deployed to block “cooptive acquisitions” and unconventional “reverse acquihires”—such as the high-profile regulatory pushbacks surrounding incumbent transactions with smaller AI firms like Inflection and Adept. Because a strategic acquisition by an incumbent cloud or software giant would face immediate antitrust litigation, an independent public IPO is the cleanest and most reliable exit path for Databricks and its institutional backers.

Macroeconomic Headwinds and Underwriting in 2026

The broader public equity markets present a highly discerning environment for these upcoming listings. The era of loose monetary policy and zero-interest-rate environments has given way to an investment culture focused intensely on sustainable cash flows, capital efficiency, and real margin expansion.

Institutional asset managers approaching these historic filings are utilizing rigorous underwriting standards that contrast sharply with previous technology cycles:

- Valuation Disconnects: Companies seeking to go public must bridge the gap between peak private valuations achieved during late-stage venture rounds and the realistic cash-flow multiples accepted by public market public fund managers.

- Dual-Class Share Governance: The public markets are increasingly demanding transparency regarding dual-class share structures, which founders frequently use to maintain absolute voting control while offloading financial risk to public retail investors.

- Geopolitical and Supply Chain Risk: For hardware and infrastructure-heavy entities like SpaceX and frontier AI datacenters, public filings require exhaustive disclosures regarding supply chain resilience, semiconductor dependencies, and international national security compliance.

Ultimately, the upcoming IPO pipeline for SpaceX, OpenAI, Stripe, and Databricks will serve as a definitive barometer for the global financial ecosystem. If these market transitions are managed successfully, they will unlock a massive wave of public liquidity, recycling institutional capital back into the next generation of venture-backed innovation. If they falter due to structural misalignments or aggressive valuations, it will signal a prolonged period of recalibration for how deep tech, digital platforms, and private capital intersect.

Sources and Links:

- arXiv (Preprint): The End of the Foundation Model Era: Open-Weight Models, Sovereign AI, and Inference as Infrastructure (Jared James Grogan, 2026) — https://arxiv.org/pdf/2604.06217

- Arizona State Law Journal: Aligned Structuring of AI Startups (Gad Weiss, 2026) — https://arizonastatelawjournal.org/wp-content/uploads/2026/05/Weiss_58-1_PUB.pdf

- The University of Chicago Law Review: When a Mass Resignation Becomes a Merger: Rethinking Asset Acquisitions for the AI Era (N. Fridman, 2026) — https://lawreview.uchicago.edu/sites/default/files/2026-06/Fridman_CMT%20-%20FINAL.pdf

- Taylor & Francis (Politics and Governance): Digital Sovereignism: A Comparative Analysis of Italian Parties’ Positioning on Transnational Data Governance (M. Griffini, 2025/2026) — https://www.cogitatiopress.com/politicsandgovernance/article/viewFile/10575/4708

- Taylor & Francis (Review of International Political Economy): Asian platform capital: An overview (A. Athique, 2026) — https://www.tandfonline.com/doi/full/10.1080/03085147.2026.2640740

- MDPI (World Journal): Network Data Maps on Entrepreneurial Intention, Unicorns, and Human Flourishing on the SCOPUS Database: A Visual Analysis Using VOSviewer (José Manuel Saiz-Alvarez, 2022) — https://www.mdpi.com/2673-4060/3/4/45

Disclaimer

Artificial Intelligence Disclosure & Legal Disclaimer

AI Content Policy.

To provide our readers with timely and comprehensive coverage, South Florida Reporter uses artificial intelligence (AI) to assist in producing certain articles and visual content.

Articles: AI may be used to assist in research, structural drafting, or data analysis. All AI-assisted text is reviewed and edited by our team to ensure accuracy and adherence to our editorial standards.

Images: Any imagery generated or significantly altered by AI is clearly marked with a disclaimer or watermark to distinguish it from traditional photography or editorial illustrations.

General Disclaimer

The information contained in South Florida Reporter is for general information purposes only.

South Florida Reporter assumes no responsibility for errors or omissions in the contents of the Service. In no event shall South Florida Reporter be liable for any special, direct, indirect, consequential, or incidental damages or any damages whatsoever, whether in an action of contract, negligence or other tort, arising out of or in connection with the use of the Service or the contents of the Service.

The Company reserves the right to make additions, deletions, or modifications to the contents of the Service at any time without prior notice. The Company does not warrant that the Service is free of viruses or other harmful components.

")

{kind=link}