In 2022, news that 27 of Florida’s property insurance companies were potentially facing a financial rating downgrade from Demotech, the state’s primary financial rating firm, created panic in the already shaky Florida insurance market.

Since then, there has been a flurry of activity from Florida lawmakers to stop private insurance companies from exiting the state and to keep Citizens Insurance solvent while trying to make it through another active hurricane season. It has been over a year and a half since Demotech’s announcement and while there have been significant changes regarding Florida homeowners insurance, Demotech only downgraded a handful of carriers.

- * Over the past two years, only nine of the 27 Florida property insurers projected to face potential downgrades had rating downgrades or withdrawals. * Freddie Mac and Fannie Mae now accept a financial stability rating of BBB from Kroll Bond Rating Agency in addition to Demotechs A rating. * Florida has passed a total of 10 new laws in an effort to make the Florida insurance market more desirable for private insurance companies.

A financial stability rating (FSR) is a score or grade assigned to an insurance company that indicates its historical financial strength and ability to honor claims. The better the score, the more financially sound the carrier has historically been.

Homeowners in Florida have limited choices regarding the carriers they have access to for home insurance. Financial analyses and rating agencies like AM Best and Demotech provide a valuable service that helps homeowners feel more confident that an insurance company will have the funds available when a catastrophic loss occurs.

Mortgage companies also rely on financial strength ratings to protect their financial interest in your home. If you have a federally-backed mortgage, like Freddie Mac or Fannie Mae, your insurance company must have an acceptable FSR rating to meet the requirements on your mortgage contract. An FSR downgrade could put you at risk of force-placed insurance, which is much more expensive than standard home insurance. In a state like Florida where carrier availability is already limited, the news of 27 potential insurance company downgrades was terrifying to homeowners.

Did Demotech downgrade 27 insurance companies?

In late July 2022, Demotech sent preliminary letters to 27 Florida-based insurance companies warning that its FSR could drop from an A (Excellent) rating to S (Substantial) or M (Moderate). One month later, three companies had rating changes and as of 2024, several more carriers have had ratings withdrawn.

On August 1, 2022, Demotech downgraded the FSR for United Property and Casualty Insurance (UPC) from an A to M and subsequently, UPC was declared insolvent on February 6, 2023. Demotech downgraded FedNat’s FSR from A to S in April 2022 and withdrew its rating in August — this company was also declared insolvent by the Florida Office of Insurance Regulation on September 27, 2022.

Additionally, Weston Property & Casualty Insurance was declared insolvent on August 4, 2022, after its FSR was withdrawn by Demotech. A rating withdrawal can often be the first step toward bankruptcy, but not always. Rating withdrawals can be initiated by Demotech or the entity under review, which happened with a few other insurance providers. See the table below for a list of insurance companies with Demotech FSR downgrades or rating withdrawals between April 2022 and the present.

| Company Name | FSR status change company | y status |

|---|---|---|

| Bankers Specialty Insurance | FSR withdrawn | Solvent – pulled business from Florida |

| FedNat Insurance Company | FSR downgrade from A to S, FSR withdrawn | Declared insolvent on September 27, 2022 |

| First Community Insurance | FSR withdrawn | Solvent – pulled business from Florida |

| Frontline Insurance Unlimited Co. and First Protective Insurance Company (FPIC) | FSR withdrawn | Solvent – still active in Florida |

| Lighthouse Property Insurance Corporation and Lighthouse Excalibur Insurance Company | FSR withdrawn | Declared insolvent on April 28, 2022 |

| Olympus Insurance | FSR withdrawn | Solvent – still active in Florida |

| Southern Fidelity Insurance Company | FSR withdrawn | Declared insolvent on June 15, 2022 |

| United Property and Casualty Insurance (UPC) | FSR downgrade from A to M, FSR withdrawn | Declared insolvent on February 27, 2023 |

| Weston Property & Casualty Insurance | FSR withdrawn | Declared insolvent on August 4, 2022 |

FSR downgrades and carrier insolvencies impacts all Florida homeowners

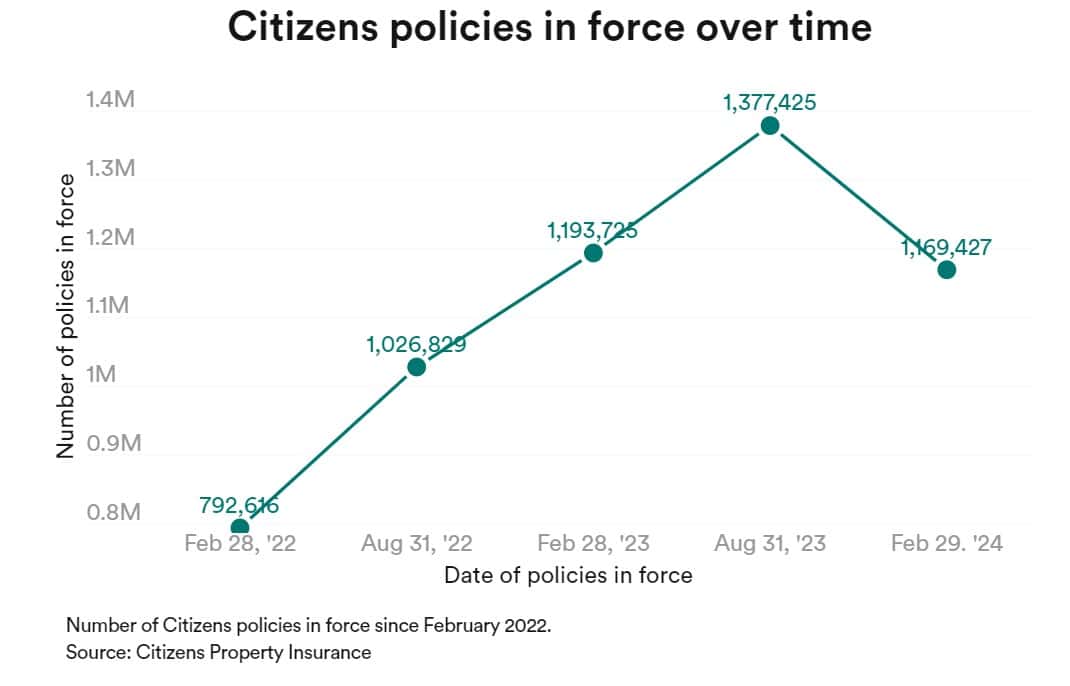

Since Citizens is a not-for-profit insurance company backed by the state, the goal is to serve as a safety net for homeowners who cannot secure coverage in the standard market. Florida has been struggling to keep private insurance companies in the state for years, and as more carriers exit the state and become insolvent, the “carrier of last resort” has been left to absorb a staggering amount of policies.

Between February 2022 and September 2023, Citizens took on an additional 615,189 new policies. The carriers that remain in the state have had significant rate increases due to rising inflation, increased costs from extreme weather and assumption of higher risk due to fewer carriers available to share the financial burden from potential loss.

Citizens hurricane tax

State law allows Citizens to obtain funding through policyholder premiums and in some circumstances, a statewide assessment, as a way to keep Citizens solvent.

If Citizens experiences a deficit, Florida law requires a Citizens Policyholder Surcharge, sometimes called the “hurricane tax”, to be imposed on policyholders in addition to their standard premium. This fee caps at 15 percent per policy for Citizens policyholders, and a statewide fee up to 2 percent can be assessed for policyholders with private carriers on all auto, condo, renters and homeowners policies in Florida. Additionally, an emergency assessment of up to 10 percent per year can be levied on both Citizens and private policyholders if the surcharge and assessments are not sufficient.

Demotech downgrade scare prompts massive changes

Even though only a few insurance companies were initially impacted by rating changes, Demotech had sounded the alarm on how problematic and fragile the Florida insurance industry truly is in the course of its standard rating practices.

The Florida Office of Insurance Regulation (OIR) originally stated that Citizens, Florida’s state-backed insurer, would serve as reinsurance for companies downgraded by Demotech. This temporary arrangement met Freddie Mac’s and Fannie Mae’s insurance requirements and put homeowners at ease. However, this is not a sustainable solution and the measure expired on June 1, 2023.

In May 2022, a special legislative session was called to specifically address property insurance concerns. However, after Demotech’s final FSR reports were announced, this prompted another special session in December 2022. The Florida legislature passed 10 additional laws impacting property insurance, two of which involved reinsurance.

RAP, the Reinsurance to Assist Policyholders fund, is available to financially sound insurers participating in the Florida Hurricane Catastrophe Fund (FHCF) and Citizens. This program reimburses up to 90 percent of an insurer’s covered losses at no additional cost. RAP is set to expire on July 1, 2025, if General Revenue funds are not transferred to the program, or on July 1, 2029, if the program is refunded.

The Florida Optional Reinsurance Assistance (FORA) Program enhances the coverage offered by RAP at premiums set drastically lower than the current reinsurance market rates. This program is set to expire on July 1, 2026, without further funding. If the program receives funding by June 30, 2026, it will continue until July 1, 2030.

Currently, only three insurance companies have elected to participate in the FORA program.

Cautious optimism

Florida’s insurance market is still uncertain, but legislators continue to push for change. On March 8, 2024, the state approved three additional bills that may save homeowners money by eliminating certain taxes and providing funds for improvement grants. While Governor Ron DeSantis has yet to sign or veto these bills, the expectation is that he will soon.

Due to some of the new laws Florida legislatures enacted in prior legislative sessions, several new insurance companies have been authorized to write home insurance in Florida. With the influx of new carriers, Citizens is working to depopulate and move about 300,000 policies back to private insurers.

Ultimately the goal is to move as many policies back into the private insurance market, which will reduce the amount of risk Citizens assumes, lower Florida home insurance premiums through increased competition and create a more stable insurance market. While it is still too soon to see if these changes create a significant reduction in premiums, homeowners in the Sunshine State have reasons to be hopeful.

“Citizens is in a much stronger financial position heading into the 2024 hurricane season compared to a year ago,” says Mark Friedlander, Director of Corporate Communication for the Insurance Information Institute (Triple-I). ”This is due to the successful depopulation of the state-backed insurer, which has moved several hundred thousand policies to the private market, reducing its risk exposure. The company has a surplus of nearly $5 billion and is forecast to grow its surplus in 2024.”

Demotech stands behind its rating process

When speaking with Bankrate in 2022, Demotech President Joe Petrelli stated that the media frenzy surrounding the rating process was unfair and misleading. “These characterizations were an inaccurate depiction of our published process and rating methodology, most significantly because they portrayed preliminary letters as if they were final, when our process — the same comprehensive process we have used for years — involves a continual review of relevant data.”

Demotech moved into the Florida insurance market in 1996 after over two dozen insurance companies became insolvent after Hurricane Andrew. Demotech’s Financial Stability Rating Methodology goes through six stages, which include reviews of a company business model, line of business risk analysis, reinsurance review and more.

Reviews can be done quarterly and annually, and if Demotech sees significant changes in operating performance, a carrier’s score can be upgraded, downgraded or withdrawn. It is standard practice for Demotech to provide the company under review with a confidential preliminary assessment before a final FSR is announced. This gives the company time to provide any additional information needed for an accurate assessment.

KBRA expands its Florida rating presence

In September 2022, the Florida legislature approved a $1.5 million plan to research financial strength rating agencies in an attempt to replace Demotech. As of yet, there have not been any changes in how Demotech is operating and it has even rated some of the new carriers to enter the Florida market, like Manatee Insurance Exchange.

However, another credit rating agency, Kroll Bond Rating Agency (KBRA) which was already providing financial strength ratings for several Florida insurance companies, is making its presence known. A few companies that withdrew from Demotch have moved to KBRA. In total, KBRA is rating 11 Florida carriers including ones entering the Florida market for 2024. “We have been in the insurance market since 2017 and I would say over the last couple of years our business has doubled, if not tripled in the amount of Florida companies we rate,” says Peter Giacone, senior managing director and head of insurance ratings at KBRA. “Some companies, like Tower Hill and Heritage, we have been rating for a while, but recently we have picked up quite a few more entities.”

In a major win for potential Florida homeowners, Freddie Mac recently joined Fannie Mae in accepting a minimal financial strength rating of BBB from KBRA — the first rating agency added to the list of accepted financial strength rating companies in 28 years. A financial strength rating of B+ from AM Best is also accepted by Freddie Mac and Fannie Mae. In a matchup of Demotech vs. AM Best and KBRA, Demotech historically rates more Florida insurance companies, but in light of Florida’s search for a different agency, that may change.

According to Giacone, homeowners benefit from there being more than one major rating agency on the scene in Florida. Oftentimes, insurance companies have ratings from more than one company, which allows homeowners to have more options — something that has been lacking in the Florida market for years. “One way we are helping the market is with start-up entities,” says Giacone. “Other rating agencies struggle with a company that doesn’t have historical data and that is not a limitation for us.”

Given the dislocations in the market, there was a desire for a different perspective. It’s not only about competition; it’s also about multiple perspectives on a nuanced area like insurance which is always a positive.

— PETER GIACONE, SENIOR MANAGING DIRECTOR AND HEAD OF INSURANCE RATINGS, KBRA

The bottom line

Florida homeowners and insurers are both eager and leery to see how all of these changes will pan out. While there was an understandable amount of concern regarding potential Demotech downgrades, the FSR changes were not what caused the carriers that became insolvent to fail — those companies were already in financial trouble and the rating changes simply reflected this. Inadvertently, the Demotech scare prompted some much-needed action from Florida lawmakers, mortgage companies and insurance companies that will hopefully pay off in the long run.

This article originally appeared here and was republished with permission.

")

")

{kind=link}